This post may contain affiliate links. Please read our disclosure for more information.

To achieve financial independence (FI), you have to save at least 25 times your annual living expenses.* For example, if it costs $25,000 a year to feed, clothe, shelter, educate, doctor, and entertain yourself, you’ll need to save $625,000. Once you’ve hit this savings multiple, you can live off the dividends and capital gains that your savings generate. Work, if you decide to work at all, will be on your terms. You’re free.

Twenty-five times your annual living expenses is a daunting number. But it’s doable. Mrs. Groovy and I did it and we made the biggest mistake you can possibly make: we started late. We didn’t start saving for retirement until we were in our early 40s.

Two important allies in the quest for FI are time and compound interest. But the later you start saving for retirement, the less helpful these allies are. Start saving in your 40s or 50s; time and compound interest will help a little. Start saving right after high school or college; time and compound interest will help a lot.

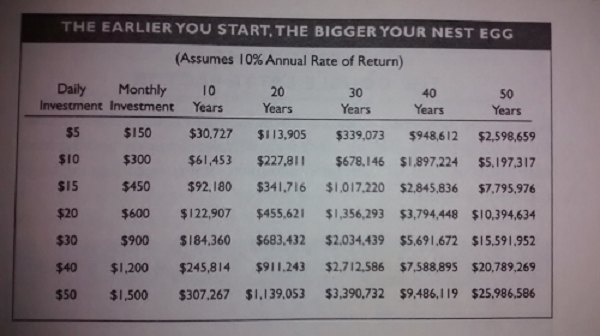

To prove how beneficial time and compound interest can be, I want you to examine the image below. It’s an image of a chart on page 39 in David Bach’s book, Start Late, Finish Rich

According to this chart, if you’re 45-years-old and save $150 a month, you’ll have $113,905 by the time you’re 65. Of this $113,905 nest egg, you would have contributed $36,000 ($150 x 12 x 20). Time and compound interest would have contributed $77,905. Not bad. Time and compound interest would have more than doubled your contribution. But if you started saving $150 a month at 25, you would have $948,612 by the time you’re 65. Your contribution to this total would be $72,000 ($150 x 12 x 40). Time and compound interest’s contribution would be $876,612—over 12 times your contribution. That’s what I call an ally.

The math behind FI is simple: 1) Spend less than you earn and invest the difference. 2) Do this consistently for whatever number of years it takes you to accumulate 25 times your annual expenses.

But while the math is simple, the execution is not. You have to workout muscles that most people prefer to neglect. For instance, you need to workout your frugal muscles. Strong frugal muscles allow you to achieve material comfort without living beyond your means (a Corolla will get you to work just as well as a Lexus will). And then there are your spartan muscles. Strong spartan muscles help you see that happiness isn’t dependant on buying every convenience or gadget known to man (life is still good without cable television). But the most important muscle of all is your saving muscle. Without saving, it’s impossible to reach FI.

The goal of this post is to help a young person begin a saving regiment. A “late starter” can certainly follow this advice, but an older person who hasn’t begun saving is in a more precarious situation and needs additional guidance. In a future post, I’ll address the needs of a late starter. For now, though, the saving regiment I’m about to propose is for someone who hasn’t begun investing and hasn’t really begun to workout his or her saving muscles. Here, then, are my working assumptions for our newbie investor:

- Age of investor: 25 or younger

- Workplace retirement plans (pension or 401K): Not available

- Initial amount to invest: less than $1,000

- Monthly contribution after initial investment: $200

- Account Type: Roth IRA

- Years to Reach FI: 30

The Workout

Okay, let’s start honing your saving muscles. Here’s the workout.

1) Go online to one of the mutual fund companies below and open a Roth IRA. Opening a Roth IRA is free.

2) Transfer your initial investment amount ($1,000 or less) from your bank account to your Roth IRA. This initial investment will be placed in a money market fund earning little or no interest.

3) Set up an automatic transfer of $200 a month from your bank account to your Roth IRA. Again, each monthly transfer of $200 will be going into your money market fund.

4) Once you have saved up the minimum amount necessary to invest in the fund designated below for your chosen mutual fund company, buy that particular fund with all the money you have in your account’s money market fund. So if you opened your Roth IRA with Schwab and have $1,000 in your money market fund, take that $1,000 and buy $1,000 worth of the Schwab Target 2045 Fund.

5) Adjust your automatic monthly transfer so the $200 goes into your chosen fund rather than your money market fund.

| Fund | Symbol | Expense Ratio | Minimum Investment Amount | Stock/Bond Ratio |

|---|---|---|---|---|

| Schwab Target 2045 Fund | SWMRX | 0.80% | $1,000 | Roughly 90/10 |

| Fund | Symbol | Expense Ratio | Minimum Investment Amount | Stock/Bond Ratio |

|---|---|---|---|---|

| Vanguard Target Retirement 2045 Fund | VTIVX | 0.18% | $1,000 | Roughly 90/10 |

FidelityFund Symbol Expense Ratio Minimum Investment Amount Stock/Bond Ratio Fidelity Freedom 2045 Fund FFFGX 0.75% $2,500 Roughly 94/6

Final Thoughts

The important thing to understand now is that this workout plan is a start. A lot of important concepts haven’t been explained. For example, what’s the difference between a Roth IRA and a traditional IRA? What does the expense ratio mean? Why are these funds weighted so heavily toward equities? What are equities? What do you do during a market correction or crash?

But knowledge of core investing concepts will come. Keep reading this blog and start reading the blogs listed on our Financial Freedom page. Personal finance isn’t rocket science. But there’s a lot to it, and it can’t be digested in one sitting. You have to take little bites over months and years before core investing concepts become second nature.

So there’s the workout. Start honing your saving muscles. Don’t wait to get time and compound interest on your side.

* Just for the record, Mrs. Groovy isn’t on board with this savings multiple. She thinks 30 times your annual expenses is necessary for FI.

Put me in the category of “late starter” for saving. I’ve always been an investor, but not a saver. Big difference. Now I’m a saver who invests as well.

The uphill battle of a late starter seems very daunting some days, but then I run a spreadsheet and remind myself that I have 20-25 years of compounding on my side. I know I can hit 10%+ returns with stocks and options, and even more with real estate, so that early retirement is still possible.

Now I just need to focus on saving as much as possible, squeezing every dollar I can out of my budget.

Great read. We setup a Roth IRA for my wife a couple years back and used the Fidelity freedom fund. We setup automatic payment and have forgot about it. It’s that easy and like you said, the earlier you start the better off you’ll be. Another great aspect I like about Fidelity is their cash back card. You get 2% cash back into a fidelity account of your choosing. So I just use my card for everyday purchases, pay it off in full at the end of the month and boom, more investing money!

Hey, Logan. Thanks for the kind words. Mrs. Groovy and I didn’t figure all this stuff out until we were in our mid-forties. We’re now nearly ten years into our financial renaissance, and it’s amazing how quickly the money adds up. The key is as you said: “setup automatic payments and forget about it.” And I didn’t know about Fidelity’s cash back card. Thanks for pointing that out. Mrs. Groovy and I will definitely check it out.