This post may contain affiliate links. Please read our disclosure for more information.

Anyone can reach chronological adulthood. You celebrate your 18th birthday and whoopee! But real adults know adulthood comes with responsibilities, such as protecting themselves and their loved ones from worst case scenarios (sh*t does happen, after all). And what is worse than death, aside from public speaking? Real adults, then, don’t shy away from their mortality. They embrace it. Real adults plan for death.

The two basic items essential to planning for death are a will and a a life insurance policy. If you don’t have these in place, here’s how you can cross them off your to-do list. You do want to become a real adult, don’t you?

Who needs a will?

Every adult should have a will, PERIOD. And if you have children, you are seriously delusional if you don’t. The last thing you want is the state making decisions about the welfare of your children. You know how government gets everything right, right?

How do I get a will?

Some experts claim DIY wills, like those from LegalZoom, are fine. But in the words of the late comedian John Pinette, “nay nay“. Get a lawyer. Legal requirements differ from state to state and it would be foolish to choose a DIY will kit for something this important.

You need a lawyer who specializes in estate planing. Find one by checking with your state Bar Association or by searching the National Association Of Estate Planners & Councils (NAEPC) website for an accredited Estate Planner or an Estate Planning Law Specialist. The NAEPC explains the difference between the professional designations, but either is good.

Start by setting up interviews (by phone or face-to-face) with two or three lawyers. Most lawyers offer a free consultation. If not, their fee is nominal and is often deducted from their bill. After the interviews, make sure you pick someone you’re comfortable with, as you will be sharing very private and delicate information.

For years Mr. Groovy and I procrastinated on getting our wills done. But then we experienced an extremely turbulent flight into Bozeman, Montana. It’s funny how impending doom can light a fire under you, isn’t it? We got cracking on our wills as soon as we returned. I can’t say the process was a breeze, but it wasn’t particularly difficult. And when it was all over, we gave ourselves a big pat on the back for finally conquering the last obstacle to becoming real adults.

Who will safeguard your will?

Your lawyer will keep the original and file a copy with the appropriate state court. You should also provide a copy to your executor, or at least make sure he or she knows where to find it. Also make sure your executor is aware of where you keep documentation about your assets, account numbers, passwords, etc. Finally, keep a copy for yourself in a safe, accessible place, like a file cabinet or a home safe. Don’t keep it in a safe deposit box because a court order may be required to retrieve it when you die. Mr. Groovy and I keep ours in a small home safe we leave unlocked.

What effect does moving to another state have on my will?

Be aware if you move to another state, you need to verify whether your will is valid in that state and/or if you need to take additional steps to make it valid. If several years have passed, you might want to create a new will.

Who needs term life insurance?

If anyone depends on you for income, or for the services you provide (e.g., childcare, running a household, etc.), you need life insurance. Not whole life insurance, term life insurance. Whole life is an investment tool. Don’t combine investing with insurance. With term life insurance, your yearly premiums remain the same for the life of the policy, and policies are typically offered for spans of twenty or thirty years.

We all know childcare is expensive and I want to stress, for couples with one working parent, it is a mistake to not insure the stay-at-home parent (SAHP). If the SAHP dies, it will be difficult for the surviving parent to pay for childcare and run a household with his or her existing income.

How much money should I insure for?

There are many factors to consider when deciding on the value of your policy. Do you have children? Will they go to college? How much do you owe on your mortgage? What does it cost to maintain your household? One rule of thumb is to get coverage equal to ten times your annual income. Mr. Groovy and I each chose 20-year term policies equal to five times our salaries. We have investments, we have no children or college educations to fund, and we have no mortgage. We also began planning in our 40s. Next year when we retire we’ll probably cancel our policies.

What company should I buy term life insurance from?

AM Best has been issuing credit ratings to insurance carriers for decades. Its ratings are usually listed on the home page of an insurance company’s website. They range from Triple A (exceptional) to C (poor). Don’t chose anything lower than an A and look for companies that have been in business since you were born: Met Life, American General, Prudential, etc, are all excellent choices.

What does term life insurance cost?

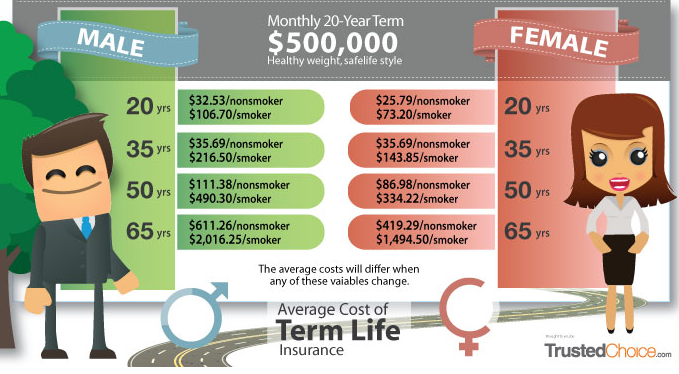

Term life insurance is relatively inexpensive, and the younger and healthier you are, the cheaper it is. It also costs less for females than for males because, statistically speaking, women live longer.

I ran the numbers on Met Life’s website for a 30-year old man and woman in excellent health. A $500,000 20-year term policy would cost $30.99/month for a man and $25.99/month for a woman. A discount is often given for paying the yearly premium all at once.

At TrustedChoice.com you’ll find the average cost of a $500,000, 20-year term policy for men and women ranging in age from 20 to 65 years old. It’s common to insure yourself on up through the end of your working life, or until your children are grown.

How do I get a term life policy?

First you’ll want to get policy quotes. You may contact insurance companies directly, through a broker, or at an aggregate site like SelectQuote that gathers information from various insurance companies for comparison.. Beware though. You may be deluged with emails and phone calls if you fill out its online form. To safeguard yourself from bombardment, set up an alternative email account and omit your phone number.

After comparing quotes, you’ll decide on a company and policy, and request an application. The application will require your medical history and health information about your parents and siblings. After you submit the application you’ll be scheduled for a physical exam. The insurer may choose the medical office, or send a nurse to your home. When Mr. Groovy and I applied for our policies the nurse came to us. She even schlepped a portable scale to weigh us (oh joy).

When you’ve completed the physical exam, an insurance rep will probably call you to verify a few facts and ask additional questions. Then you wait for approval. An insurance underwriter will evaluate you for potential risk to help determine the final cost of your policy. If the information you’ve provided, medical facts and results of your exam are all in sync, the quote you received should be fairly accurate. Finally, the policy will be sent to you for review, signature, and payment.

Note, you are not agreeing to purchase a policy when you request an application. You may apply to several insurance companies simultaneously to see which one offers the better price in the end. Also, at no point should you provide any false information. If you’re a smoker, be honest. If you indicate you don’t smoke and the insurer finds out otherwise, your policy may be cancelled and any premiums you have paid will not be reimbursed.

Final Words of Wisdom

I know this isn’t exactly a fun topic for Thanksgiving. Planning for death is not nearly as palatable as Aunt Martha’s green bean casserole or Cousin Betty’s sweet potato pie. So have a wonderful Thanksgiving with your family. But after you’ve awakened from your food-induced coma, make it a serious priority to get a will and life insurance policy. You’ll feel extra groovy knowing that you and your loved ones are protected.

Wills and life insurance are important, and so is letting your family know your wishes for end of life care. I hope it will never be more than a hypothetical question, but would you want life support in the form of a ventilator, CPR, a feeding tube, etc?

Hard situations are so much easier on family when they know what you want than when they have to guess, decide for themselves, and feel guilty about the decision.

A POA and a living will are helpful, but actual conversations with your next of kin are priceless.

Definitely, we’ve talked about it with each other but it wouldn’t hurt to have a more in depth conversation with my brother and Mr. Groovy’s sister – who are our back-up executors.

Do you see people at the hospital using the Three Wishes document as a substitute for the living will? It’s legal in most states and it’s free. For those reluctant (or not easily transportable) to a lawyer, especially the elderly, I think it’s a good tool

An interesting thing happens when you accept mortality – you appreciate life more and reprioritize how you spend your time because you realize how precious it really is and don’t want to waste it on meaningless crap.

Thanks for your comment, Ty. Mortality can be a vague concept. That is, until you start losing people close to you. I wish I could always do as Tim McGraw recommends in “Live Like You Were Dying” but at least I’m getting better at it.

Lots discussion about this in Minneapolis right now. The newspapers are writing articles about Prince’s passing and where his estate is likely to end up.

Wow I didn’t realize that. There are so many stories about people with gobs of wealth who didn’t make the proper arrangements. What really gets to me are the tales I’ve heard about parents with more than 1 child, who leave everything to only 1 child (usually the oldest) thinking the children will naturally share equally. That’s a recipe for tearing a family apart.