This post may contain affiliate links. Please read our disclosure for more information.

I’m a big fan of Barry Ritholtz. For those of you who are unfamiliar with him, he’s the Chief Investment Officer of an asset management firm he founded and a frequent contributor to Bloomberg View and the Washington Post. He also has a blog called, The Big Picture.

In his most recent WaPo contribution, he discusses the difference between investing by outcome and investing by process. Those who invest by outcome are very driven by returns—they gotta beat the market. And because they’re fixated on returns, they become very reactive investors. When the market gets ugly, they rush for the exits. When the market is careening toward new highs, they pile in. And when they’re not trying to time the market, they’re chasing the hot fund manager, the hot stock, or the hot investing fad.

Investing by outcome is an exercise in futility. No one knows when the market will peak or when it will bottom out. Those who try to time the market are more apt to get it wrong than right; that is, they’re more apt to buy when stocks are overpriced and sell when stocks are undervalued. Chasing what’s hot doesn’t work too well either. The hot fund managers of 2015 will almost assuredly not be the hot fund managers of 2016. And the same goes for stocks. Just a couple of years ago, 3D printing stocks were all the rage. But those who bought into the hype got creamed. Stratasys, for instance, one of the companies at the center of the 3D printing hoopla, has seen its stock price fall nearly 90 percent since January 2014 ($136.46 per share to $16.30).

So forget about investing by outcome. Invest by process. “Okay,” you’re no doubt saying, “I’m all for investing by process. What the heck is it?” In a nutshell, it’s a plan. You devise action items a, b, c, and d, and you follow these action items no matter what the market is doing. If the market’s crashing, you’re still doing a, b, c, and d. If the market’s on a tear, ditto—a, b, c, and d. You’re behavior doesn’t change. You follow the plan. But here’s the key. The plan you devise must do the following:

- Keep you invested in the market for the long haul.

- Increase the likelihood that you’ll buy low and sell high.

- Protect your investments from your irrational self (e.g., trying to time the market, chasing the hottest fund, etc.).

If your plan accomplishes the above, you got a good process. You won’t earn spectacular returns. You’ll only get average returns (6-7%). But average returns produce awesome results if allowed to accumulate over time. And, besides, you’ll do far better than the guys investing by outcome.

Mrs. Groovy and I didn’t invent our process overnight. It took a while for us to get out from under the investing-by-outcome mindset. But, with the help of such luminaries as Jack Bogle, Dave Ramsey, and David Bach, we managed to cobble together a process that works for us. And here it is. I hope it can help you formulate your own.

The Groovy Investing Process

Invest a certain amount every month (dollar-cost averaging)

Every month, Mrs. Groovy and I dedicate a certain percentage of our paychecks to fund our 401(k), 403(b), and Roth IRAs. This is a great way to instill discipline and make sure we continue to buy stocks and bonds when they’re on sale. Market down + same monthly contributions = more shares purchased.

Automate monthly contributions

By automating our contributions to our retirement accounts we do two things. First, we force ourselves to live on less. Contributions come right out of our paychecks like a mortgage payment or an electric bill. We have no choice but to make due with what’s left over. Second, we give our discipline muscles a break. Once automation was set up, making our monthly contributions became effortless.

Maintain a 60/40 asset allocation between stocks and bonds/cash.

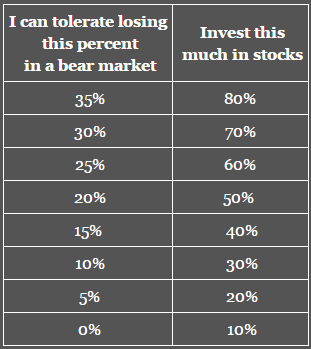

This action item is key. The more stocks you have in your portfolio, the more it will be subject to dramatic drops. How much of a drop could you handle before crying uncle and frantically clicking the sell button? Dirk Cotton over at the Retirement Cafe recently posted this chart from William Bernstein’s, The Four Pillars of Investing

I’m a wuss. I’d like to go to a 50/50 or a 40/60 split by the end of this year. But Mrs. Groovy is very comfortable with a 60/40 split. She has ice in her veins when it comes to investing. And that’s fine. We’ll stick with 60/40. As long as she can handle it, I’ll suck it up during the next market crash.

Maintain the following asset class percentages in our portfolio.

The goal here is to minimize risk by diversifying. We think we have a nice mix of asset classes. Our only concern is the lack of an emerging market stock fund and a short-term US bond fund.

Stocks

- US Large Cap: 40%

- US Mid Cap: 10%

- US Small Cap: 10%

- Energy: 10%

- REITs: 10%

- International Developed: 20%

Bonds/Cash

- US Intermediate: 60%

- Corporate High Yield: 16%

- Emerging Markets: 8%

- Cash: 16%

Don’t watch CNBC and the daily fluctuations of the market.

Just before the new year we stopped watching financial news. We couldn’t have chosen a better time to shun the media. We hear the market has dropped ten percent or so since January 1. But because we don’t partake in financial news anymore, we really don’t know. And we don’t care.

Check portfolio every December for tax-loss harvesting opportunities.

This past December we sold a number of shares of our energy fund for a loss. This loss, in turn, reduced our 2015 tax liability. A month and a day after we sold those shares, we used the money from that sale to buy back as many shares as possible of the same energy fund. And because oil prices continued to fall in the interim, we were able to buy more shares than we sold.

Rebalance every January.

This is another great way to systematically buy low and sell high. If our stock funds have a great year and our portfolio goes from a 60/40 split to a 70/30, we sell enough stocks and buy enough bonds to get back to the 60/40 split. By following the plan, we’re selling stocks when they’re high and buying bonds when they’re low. This is quite possibly the only free lunch in the investing world.

Have at least three years of expenses in cash.

This is the main reason why I don’t push back against Mrs. Groovy’s preference for a 60/40 portfolio (and you thought it was because I wear a dress!).

Make sure we have enough bonds and REITs in our non-tax advantaged brokerage accounts to generate $12-15K annually in dividends.

The $12-15K in dividends we’ll get from our brokerage accounts will be used primarily to fund our health saving accounts (HSA) in retirement.

Do not reinvest our non-tax advantaged brokerage account dividends. Use to max out HSA contributions.

The current HSA contribution limit is $4,350 (if you’re 55 or over). Mrs. Groovy and I will thus need $8,700 to max out our HSAs.

If we do invest in an individual stock, we only invest an amount we can afford to lose (no more than two percent of our portfolio).

Mrs. Groovy and I are currently invested in a stock called Western Lithium. It’s supposedly developing lithium mines in Argentina and Nevada. Now, in all likelihood, this penny stock will crash and burn. And if that’s the case, no biggie. We only invested an amount of money we could afford to lose. But if its management somehow pulls it off and manages to become the principle lithium supplier to Tesla’s gigafactory, I’m having groovapalooza at my house, and you’re all freakin’ invited.

Any stock purchased must be held for at least a year.

This action item is used to instill discipline and avoid the tax rate of short-term capital gains.

After the waiting period, we should only consider selling the stock if its price has at least doubled.

Western Lithium is our lottery ticket. Selling it for anything less than twice our purchase price will not materially alter our financial picture. So we’re going to hold out at least until 2020 and see if we can bag a mega profit with this puppy ($200-$300K).

Final Thoughts

There you have it groovy freedomists. That’s our process. What do you think? What about your process? Would you like to share it?

I love this investing philosophy! You guys do a great job of taking out a lot of the behavioral aspect of investing that makes most people suck at investing, namely by automating and sticking to a certain allocation despite what the market is doing. I recently automated all my investing as well because I get too jittery trying to time the next market drop, which no one can possibly do. Great advice here 🙂

Definitely important to have a system that works for you and takes your emotions out of things.

I wish I had more regular income so that autopay worked for me. For now, I monitor like a hawk.

Once I’m far closer to free, I’ll probably try the under 2% lottery ticket/Individual stock idea.

Maxing out HSAs as part of a plan is something that I didn’t have before my rat race escape. That is a good point for people (like me) who wouldn’t naturally think about it. Nice list and certainly simple enough that anyone could apply it to their own FIRE journey.

My company just recently introduced the HSA. And after looking at it, and it’s triple tax-free advantages, it was a no-brainer. It would be foolish not to take advantage of it. I would encourage anyone who has minimal health care issues to jump on it. Thanks for stopping by, Tommy.

I think dollar cost averaging is great. My husband uses special charts to assess future trends in the market, but we never try to time the market. We are in it for the long haul. I am more than ok losing a bit of money now for biggere returns in the future. Thanks for the great advice.

Hey, Pamela. Love your attitude. It took Mrs. Groovy and I a while to understand that “losing” money was part of the process. Now we see market corrections as buying opportunities. Be greedy when others are fearful! It looks like you and your husband learned this lesson a lot sooner than Mrs. Groovy and I did. Thanks for stopping by, and thanks for your kind words.

That’s a really well developed investment plan. I need to develop a more sophisticated plan, because right now my active investment choices have been to move from higher fee mutual funds to lower cost index funds, to have a solid portfolio of high dividend yield stocks where all dividends are reinvested, and to use muni bond interest to bulk up cash reserves and occasionally pick a new stock. But I have no plan for selling and don’t manage my rebalancing as well as I might.

Hey, Emily. Thanks for stopping by. And thanks for your kind words. What’s really helped us is getting our investment plan down on paper (or on a computer screen, actually). It makes us think about it more. Is our process sound? Where are the weak spots? And we refer to it every time we make a decision. It helps us avoid being too emotional. I like where you’re going with your portfolio. Mrs. Groovy and I are definitely low-cost index fund people. But I like your idea of dividend stocks. In this era of low interest rates, they’re a nice substitute for bonds. And my cousin, who is an estate planning advisor at Merrill Lynch, is a big proponent of municipal bonds. So Mrs. Groovy and I are doing our homework. We may add muni bonds to our portfolio during our next re-balancing. The plot thickens.

I couldn’t agree month with regular monthly investing. I don’t have a lot of time to research stocks so I have a similar approach with monthly deposits into ETF’s. Can’t complain about the returns over the last 8 years!

I would like to buy a few more individual stocks though, Just for the excitement of choosing something myself. I’ve been tracking a couple of companies and at the moment they look like a good buy. They aren’t penny stocks but a local company that builds and runs upscale retirement villages here and in Australia.Only looking at 3% portfolio allocation though, like you guys I don’t want to get carried away!

Hey, QWFL. Thanks for sharing. Yes, the last 8 years has been pretty good. And I hear ya about individual stocks. You can’t be boring all the time. A little excitement is good. Mrs. Groovy and I will pick an individual stock every few years. Western Lithium is our latest adventure. Good luck with the retirement village. The world is aging, especially in the developed world, and most things catering to the elderly should see solid growth (healthcare, cleaning services, senior housing, etc.). Let me know if you pull the trigger on that stock. I’m curious to see how it works out.

P.S. I love your work selfies.

One of my 2016 goals is to get more savvy with my investing. Certainly not in the stock picking sense, but merely continuing to diversify my options (currently just invested in index funds) as well as figure out how much I’m comfortable having in the market verse in cash consider mid-term goals, like buying a house in 3-5 years. I appreciate you sharing your strategy. RE: Your Lithium investment, you should google my Dad, “Mr. Lithium”, no joke. Real name is Joe Lowry of Global Lithium LLC.

Shut the back door! I just discovered your dad last month. He’s been interviewed a lot lately. I guess that’s what happens when you’re Mr. Lithium and the price of lithium is exploding. For anyone interested in lithium, he’s a great resource. And congratulations on your 2016 goals. When I was your age, I think my goal was to drink more beer and eat more bar pies. I’m sure it seems so daunting now, but you’re way ahead in the game of money. Just stick to low-cost index funds (I love Vanguard) and you’ll be fine. Twenty years from now you’ll look at your portfolio and wonder where did all that freakin’ money come from. Thanks for stopping by. And say hello to your dad for me!

Great post. Nice simple advice that everyone should follow (and we have for 25+ years). It’s made a huge difference. While I think it would be fun to portion off a small amount of our money and test my prowess as a pretend ‘day trader’ – it would have to be only a token amount for me.

Hey, Mr. FS. Slow and steady. Be boring. As an investment strategy, it has certainly worked for us. And I get what you’re saying about day trading. Nothing wrong with a little gambling as long as you’re gambling little. It adds a some spice to one’s life.

Mr. Groovy, I am not an investor, but I watch CNBC, Fox Business. I like knowing what is coming in business. I agree you need to be a long term investor rather than concentrating on the results.

Thanks for stopping by, Michael. I used to watch CNBC all the time. But market fluctuations were becoming too distracting so I decided to go cold turkey. So far, so good. We’ll see what happens.