This post may contain affiliate links. Please read our disclosure for more information.

Prior to my fortieth birthday (I’m 55 now), I was a financial moron. I wasn’t good at making money, and I wasn’t good at saving money. My financial IQ was appalling. Rudimentary financial concepts such as “pay yourself first,” “build an emergency fund,” “automate your savings,” and “invest in low-cost index funds” were utterly alien.

And the truly sad part is that I was only vaguely aware of my financial inadequacies. Nearly all of my friends were doing better than I was, but I chalked this up to dumb luck. They just happened to stumble upon jobs and careers that were more remunerative. There was really nothing wrong with me.

Or was there? Enter my coworker Anthony.

Anthony was the same age as me and held the same job title. He wasn’t a rocket scientist, but he certainly wasn’t a dolt. And he certainly wasn’t a dolt when it came to finances. He had a landscaping side-hustle and a voracious appetite for saving. Buy the time his fortieth birthday rolled around, he was a millionaire.

Now here’s a rather inconvenient question. Since Anthony and I both made the same amount of money at our principal jobs, and since I had just as many opportunities as he did to improve my financial position, why was he a millionaire and I a nothingaire? There’s just no getting around it: I was a full-blown financial moron.

So what about you? Are you a financial moron? You might be. But then again, you might not be. The only way to know for sure is to first gather the information needed to diagnose a case of financial moronity. Let me show you how.

Gather the Key Data

To diagnose a case of financial moronity, we need four pieces of information. Here they are.

1. Monthly income. This is the income you bring in every month. Because Mrs. Groovy and I are retired, our monthly income is derived from a small government pension and a very conservative safe withdrawal rate from our portfolio. It amounts to $3,600 per month.

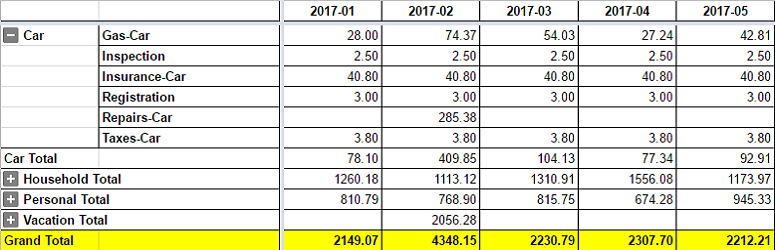

2. Monthly expenses. This is what you spend every month. To track our spending, Mrs. Groovy and I use a simple spreadsheet in Google Docs. (If you want to try it, here’s the link to download it.) I provided a screen shot of our spending spreadsheet below. Notice how the Car category’s subcategories are displayed? I did this to show how annual bills, such as our car registration bill, are broken down into their monthly equivalents. I suggest doing this with all your annual bills for two reasons. First, it gives you a more accurate accounting of your monthly spending, and, second, it helps you account for all of your spending. Bills you only pay once or twice a year are easily forgotten.

3. The gap. This is the difference between your monthly income and your monthly expenses. Our gap this year is averaging $950 per month (see screen shot below). If this keeps up, we’re going to have one hell of a Groovypaloosa at the end of the year.

4. Net worth. Add all of your assets (savings, investments, car, boat, house, etc.) and subtract all of your liabilities (credit card debt, car loan, mortgage, etc.). The difference is your net worth.

Track Your Progress

Now that you know the data necessary to diagnose a case of financial moronity, start tracking this information. Every month calculate your income, your expenses, your gap, and your net worth, and put those calculations into a spreadsheet. At first, this bookkeeping will be annoying. But as you develop your tracking spreadsheet, and as you tailor your tracking spreadsheet to your peculiar needs and circumstances, this chore will becoming easier and easier. I spend less than an hour a month tracking this information.

Okay, you set up your tracking spreadsheet and you’re faithfully recording your key financial data every month. What does it all mean? How will all this help you determine if you’re a financial moron?

In general, as you track your data from one year to the next, you want your monthly income to be growing, your monthly expenses to be stable or shrinking, your gap to be positive and growing, and your net worth to be growing. If this is what actually transpires in your financial life, leave things alone. Whatever you’re doing, it’s working. You’re as far removed from being a financial moron as possible.

On the other hand, if this isn’t what actually transpires—you can’t seem to make any financial headway when it comes to your income, expenses, gap, and net worth—then something’s wrong. You may not be a financial moron, but you should be worried.

Be Brutally Honest with Yourself

Life is messy. Housing markets collapse. Jobs migrate across the country and across the world. Cars break down. Illnesses devour emergency funds. So it’s highly unlikely that your income or net worth is going to increase every year for decades on end. You will have setbacks. And that’s okay. The trick is to avoid several years of setbacks in a row.

To gauge how you’re doing, I recommend scoring just your gap and your net worth. Compare the current six or twelve month period to the previous one and use the following point system.

| Comparison of the Current Period to the Previous Period | |||

|---|---|---|---|

| Got Worse | Remained the Same | Got Better | |

| Gap | -1 | 0 | 1 |

| Net Worth | -1 | 0 | 1 |

Next, keep a tally of how your gap and net worth did during each period going forward. In the below example, I show the the gap and net worth scores of a hypothetical individual for the years 2014-16.

| Combined Score of Gap and Net Worth Scores Over Several Consecutive Years | |||

|---|---|---|---|

| Year | Gap | Net Worth | Combined Score |

| 2014 | -1 | -1 | -2 |

| 2015 | 0 | -1 | -1 |

| 2016 | 1 | 1 | 2 |

Armed with this scoring system, your goal is to have more positive combined scores than negative. If you manage to do that, you’re doing a lot of things right. If you don’t, you got problems. And if you manage to string together negative combined scores for three consecutive years, you need to seriously question your financial IQ.

Again, life is messy. I get it. Suffer a brutal car accident and your combined score could easily be negative for several years in a row. The same fate could await you if you happen to be a college student taking out student loans. But for our purposes here, you will be deemed a financial moron if, absent some clearly mitigating circumstances, you manage to get a negative combined score for three consecutive years.

Okay, using our key data and scoring system, you’ve determined that you’re a financial moron. What do you do?

First, check your financial ego. Admit to yourself that your current approach to money isn’t working. You need a better money philosophy.

Second, to get a better money philosophy, you need to educate yourself. Read ten personal finance blogs a day. And read one personal finance book a week. Then, third, as your financial education unfolds, start applying what you’ve learned. Get a part-time job to increase your income. Downsize to a smaller home or apartment to reduce your expenses. Open a Roth IRA and contribute $400 a month to an S&P 500 index fund. In short, start the process of financial de-moronification—do whatever it takes to increase the gap and become a first-rate investor.

No Excuses

“But wait a second,” I hear you howling. “What if you were born into a family and community that was awash in financial ignorance? What if you were never taught the fundamentals of personal finance? How, then, are you supposed to improve your condition and rise above the sorry state of financial moronity?”

Good question. The chains of culture are extremely hard to break. Financial moronity begets financial moronity.

But here’s why we should be very leery of this excuse.

Suppose you come across a bigot, someone who loathes those who are not part of his tribe. And let’s further suppose that this said bigot was never taught the fundamentals of brotherly love. He grew up in a family and community full of bigots. Would you give this bigot a pass? Would you say his bigotry is not his fault, and society can’t expect him to mend his foul views?

Don’t allow financial morons to use the culture card. Yes, you can’t choose the financial culture you’re born into. But financial cultures are free. If your financial culture sucks, you can choose a better one for no charge. You know what else is essentially free? Information. For practically nothing, one can go online or go to the library and quickly learn how to make more money, reduce household expenses, and become a better investor. In this day and age, there is simply no excuse for being a financial moron.

Final Thoughts

Okay, groovy freedomists, that’s all I got. What say you? Is my test for financial moronity valid? Or am I overlooking something. Let me know what you think when you get a chance. Peace.

I think that you are the opposite of a moron. You have an awesome blog that is both entertaining and educational. You had a later start than your old coworker, but still reached FIRE. We all have different starting points on this path to FI. IMO, it is about enjoying the journey and judge yourself after you reach the finish line.

Thank you, Dave. You’re much too kind. And I love your perspective on FIRE. “[E]njoy the journey and judge yourself after you reach the finish line.” One of the most poignant financial mantras I’ve heard in a while. I salute you.

Another great post, Mr. G! It wasn’t until I started tracking everything that I realized the error of my ways. Finding the personal finance community, especially the FIRE community changed my life and for that, I’m very grateful.

You don’t know, what you don’t know. But once you figure it out you sure as heck better use that knowledge and quit being a moron.

A Groovypaloosa sounds way awesome!

No confirmed bands for Groovypaloosa as of now. I’ll keep you posted. And you are so right about tracking. Just gather the information and think about it. Do those two things and you’re bound to improve your finances. De-moronification is actually quite easy. The problem, as you correctly alluded to, is that most people never realize they’re financial morons until it’s too late. Sigh.

Great way of looking at things, Mr. Groovy.

I especially like the self-assessment part. It’s one thing to put tracking systems in place – it’s a whole other thing to actually take the time to reflect on what it all means and how you want to improve!

Self-assessment isn’t easy. The ego is a powerful liar. But if you can’t produce a positive gap and your net worth is going down every year, you got to surmise that something’s wrong. I know it’s a leap, but I’m hoping my tracking system would trigger the necessary financial reflection upon three consecutive years of futility. We are truly our own worst enemies. Thanks for stopping by, Chris. It’s always a pleasure hearing from you.

It was an interesting situation in the military because everyone wears their paycheck amount on their shirt (rather literally!) so you know almost exactly what each person earns. What they made of that money was a VERY different story. I remember being about 23,24 and Mr. Mt’s coworker was complaining about his debt and their low wages. Mr. Mt explained how we had the same debt 5 years earlier but now we had 100k to our names in cash. I thought the guy was going to fall over! People tend to underestimate the amount of change they can create by being intentional and focused with their spending and saving.

“People tend to underestimate the amount of change they can create by being intentional and focused with their spending and saving.”

No further commentary from me is necessary. I hope Mr. Mt’s coworker was smart enough to use Mr. Mt as a model. Thanks for stopping by, Ms. M. I always feel better after reading your comments. There is hope for mankind.

Oh, I hope you have Groovypaloosa! 🙂

I think if you can recognize you’re a moron, that’s the very first step. The information is out there – for FREE – to learn all you need to know. You have to having the burning desire to become a non-moron and push past those excuses and cultural influences. And the spend tracking is the best place to start (love the subcategories btw!).

Couldn’t agree more. First, be strong enough to admit you’re a moron. Second, develop a voracious appetite for financial information–especially the free stuff. Finally, third, dedicate yourself to the de-moronification process and “push past [the] excuses and cultural influences.” It’s so simple. But damn, one’s ego and culture are formidable foes. Thanks for stopping by, Amanda. I love the way you get to the heart of the matter with just a few sentences. Amazing.

NIce post! I was brought up in a fairly financially ignorant household. For instance some of their advice was along the lines of “having a lot of credit card debt is fine because you can pay it off quickly once you get your job.” “Cashing out your 401k isn’t a big deal if you need it because you can replace that money easily once you get your job.”

This was the O&G job that wasn’t quite materialized yet because I only had an internship offer at the time. Aye yi yi… To be fair, I probably wouldn’t have listened to much good advice though. Although I did manage to bank $12k in a 401k before I cashed it out.

Tracking our expenses was the key for us, and having Mrs. SSC not being such an utter financial moron like me. That was more key than anything, lol. I too was an utter financial moron and like you took steps to get myself out of moron-dom. With the amount of free PF info out there, it’s really only your own fault if you don’t do something about it.

Agreed. My 20-something brain was impervious to what good advice was thrown its way. Thankfully, as I was closing in on 40, I started to wake up. Marrying Mrs. Groovy and sealed the deal and my financial renaissance began. The old saw, “behind every great man is a great women,” may not be applicable for every successful guy out there, but it was for me. It looks like you married up too. Bravo, my friend. Thanks for stopping by.

Measure, measure, measure . . . yet I admit years of this in my professional life still didn’t translate to my personal financial life until my mid-30s.

I do think some of it is learned, but alot of it is laziness and likely fear/shame of what you’ll find out. Good stuff!

“[M]ankind are more disposed to suffer…than to right themselves by abolishing the forms to which they are accustomed.”

Why is inertia the default setting of man? I think you nailed the most likely reasons. Laziness, fear, shame–they all conspire to keep us trapped in our destructive, yet comfortable routines. Meh. Thanks for stopping by, TI. You really got me thinking. Bravo.

Love the post. No nonsense, no excuses. There is so much information out there about budgeting, how to save, and cheaper alternatives for products that you can use to get the best price and keep your finances in line. Your article does a great job showing what a difference the person makes. Thanks for taking the time to put this together.

Bert

Here’s one for you, Bert. A few years ago, a void developed under a small section of our hardwood floors in the living room (we have glued down flooring). Every time you stepped on the floor above this void, you would produce a “thwoop” sound. It annoyed the crap out of me. So I went online to find a solution. Within fifteen minutes I found a repair kit that cost less than $50. Once the kit arrived, it took me about a half hour to eliminate the void. Now a question. What would I have done 20 years ago? I would have called a flooring guy, and it would have cost me hundreds of dollars to have him fix it. As you made crystal clear in your comment, Bert, we live in an information age. Any problem you want to fix–from flooring to finances–can be fixed for an extremely low cost by simply going online. The only thing that’s holding us back is our attitude. Enough of the victim mentality; enough of the excuses. Thanks for stopping by, my friend. I really appreciate your insights. Cheers.

I like it Mr. G,

Using your methodology here I was complete moron until I was 40 years old. It was then I finally smartened up and “learned to earn”, as well as how to use a spreadsheet.

But even when times are great and your monthly positive spread is more than double it’s amazing how complacent and wasteful one can get.

So when the rainy season comes….ouch.

Tweeted this with your quote “The chains of culture are extremely hard to break…”

B

It’s not fun when you realize you’re a financial moron. The human ego much prefers comfortable lies to the unvarnished truth. But where do those comfortable lies take us? Penury? Cat food for sustenance? I’m so glad I finally woke up. I just wish the blow to my ego occurred when I was 20 rather than 40. Sigh. Thanks for stopping by, Brent. It’s always great hearing from another recovering financial moron. Cheers.

That’s a sweet gap Mr. Groovy!

I haven’t experienced a decline in net worth yet but like you say market downturns happen and jobs turn sour. We have it too good right now. Makes me suspicioussss…

I’ve heard the other excuse: my parents are rich so I never learned the value of a dollar, that’s why I’m broke. Same slop just a different way of saying “I can’t be bothered.”

Whoa! I love it. “Same slop, just a different way of saying, ‘I can’t be bothered.'” A lot of wisdom there, Lily. The human capacity for self-delusion and excuse-making is boundless.

Great post Mr Groovy! It’s always amazing to me how people with the same job title / salary can have wildly different financial lives.

I’m glad you got on track when you were a young buck. On my first tour overseas, the Army Chaplain gave us a speech about putting first things first. His “first thing” was investing in the government TSP. We were all between 18 and 25 so he didn’t exactly have an engaged audience. Some people listened. Some didn’t. Those who did invest in the TSP got off to the right start, while some coworkers spent every dime.

Thank you, Matt. You are so right. Young people seem to be biologically adverse to drinking from the well of wisdom. I remember a coworker coaching me early in my career to avoid credit card debt at all costs. I remember another coworker imploring me to bank my sick time (you got a check for accrued sick time upon separation). And I remember a family member telling me to open a Vanguard IRA. Did I listen? Hell no. Their advice was perfectly sound, and I knew that. But my immature brain preferred partying and stuff to financial security. Meh. I hope you were wise enough to listen to that chaplain, my friend.

You’re right, Mr. G, there is no excuse for being a financial moron. Not when there’s a wealth of information on how to counteract that malady right here on the interwebs and in the library. From my own experience, I know that getting started, admitting that you don’t have the answers and need to find them, is probably the most difficult part. Hopefully you’ve set a few morons on their financial improvement journey today. And I’m looking forward to hearing more about Groovypaloosa!

Want to cut your grocery bill? There’s a blog for that. Want some side-hustle ideas? There’s a blog for that. Want a low-cost investment strategy for a Millennial starting his or her professional career? There’s a blog for that. The amount of quality, free financial information out there is staggering. As you so aptly pointed out, Gary, the most difficult hurtle people have today is “admitting that [they] don’t have the answers and need to find them.” Thanks for stopping by, my friend. I’ll keep you posted on Groovypaloosa.

You know, at least you made up for your rudimentary ways – most people never get around to it!! I am thankful to all the FI peeps who have come before me and shared their wisdom. Because of that, you’re right, there is no excuse!! We hide from what we don’t know because we think it is so difficult but once you read a bit it gets easier and easier to understand. You didn’t give up after stumbling your first few steps when walking so don’t give up if you stumble in the financial realm. Get up, dust yourself off, and find another way to learn.

“You didn’t give up after stumbling your first few steps when walking so don’t give up if you stumble in the financial realm.”

Thank you, Miss M. Excuses may sooth the soul but they also subsidize failure. And as the old economic saw goes, “whatever you subsidize, you get more of.” Thankfully, I finally realized that excuses weren’t my friend. It hurt to admit I was a financial moron, especially at the advanced age of 40. But dropping my excuses for financial mediocrity and failure was the best move I ever made.

I’d push this further to say that age isn’t an excuse either. I hear a lot (I mean A LOT) of people chalking it up to being in their 20s or 30s. Nope. Once you’re made aware of something, you can start making progress. And way to kick butt with maintaining that gap!

I love the cut of your jib, Penny. On D-Day, we had 19 and 20 year old men storming the beaches at Normandy. Paul Tibbets, the pilot of the plane that dropped the bomb on Hiroshima, was 29 years old on that fateful day. And, yet, a majority of our 20 and 30 somethings today can’t put $100 a month in a Roth IRA. Pathetic.

As someone who grew up in a financially ignorant home, I agree with you that there aren’t really any excuses in this day and age. What my parents couldn’t teach me, I sought out on the Internet when I grew up. I found personal finance blogs and they kicked my ass to actually do something about my situation. I learned about possibilities that I never thought could apply to people like me.

But I think there’s more to it than just financial awareness. For example, my sister and I grew up in the same exact house with the same parents. The way we handle our money couldn’t be more different. I think people’s personalities definitely predispose you to how well you “take” to financial advice.

Excellent point, TLS. My brother and I grew up in the same household with the same parents, and he was far better at making money than I. We came from a long line of civil servants, and that’s the route I took. But my brother took the entrepreneurial route. So there is definitely a gene that makes one more amenable to the fundamentals of personal finance.

Great post-Mr.G. I was in the same boat, although I didn’t have a millionaire co-worker or at least none that I knew about. We had our financial wake-up call at 40. There is no excuse for being a financial moron. Change is possible, but sometimes we need a little push in the right direction. Or at the very least some type of awakening to break the spell of the past.

Thanks, Brian. I really appreciate your kind words. Did you hear Shannon and her lady friends last week on the Martinis and Your Money? You were a prominent part of the show. They loved the financial moronity you exhibited early in your adult life.

I heard. At least I finally made a happy hour episode!

Haha! Even though Shannon and the gang were using you as a Mexican pinata, you could tell they were doing it out of love.

It’s a pretty good start. I might add a step to ensure you know what your goals actually are. How can you sail on the ship called life if you do not know where your headed at least at a cursory level?

If your truly driven towards those goals and yet you grew up with less then adequate role models, then you should use what you saw not working as a driver to succeed. I grew up with parents who I’d still categorize as financial morons. I watched, observed what didn’t work, and applied it as motivation to ensure I did not make the same mistakes.

Excellent point, FTF. Without goals, all that gap-building and net-worth growing can be pretty meaningless. And I love how you used your parents as anti-models. The common route is to find a good model and do exactly what he or she is doing. It takes a special mind to do the opposite–find a bad model and do exactly what he or she isn’t doing. Bravo, my friend.

I was born into a family awashed with financial ignorance =) but luckily my parents were super conservative with money. So at least I had that growing up. I read some great investing-related books early in my life and met some great mentors along the way. Have been investing since my late teens. The 2008-2009 crash was a massive boon for me!

That’s awesome, TK. From your parents you learned how to “live within your means,” and from your curiosity you learned the fundamentals of investing. And all in time to put you in a great position to capitalize on the 2008-2009 crash. “Be greedy when others are fearful.” Thanks for stopping by, my friend. I really appreciate what you had to share.

It makes sense, are you saving more than you are spending? +1. Are you growing your net worth? +2.

Would it be possible to have a +1 for the gap and a -1 for your net worth? I guess if you took out unsecured debt, but other than that, I’m not sure .

Hey, Erik. I was thinking along the same lines. How many possible scenarios are there? In 2008, for instance, my gap improved but my net worth took a hit because of the Great Recession. And I suppose if I got hit with an unexpected medical bill during a great Wall Street rally, my gap could decrease and my net worth could go up. So I definitely think a +1/-1 and a -1/+1 could happen. Whew. This personal finance stuff is hard. Thanks for stopping by, my friend.

The interesting part I think is that many financial morons don’t know or don’t believe they are. They grow up in perceived wealth. They have all the stuff their little hearts always desired because mommy and daddy gave it to them. They may have missed the signs of parents worrying, being able to pay the $6,000 mortgage, start of next month.

I like the idea of your diagnosis.

Agreed. Self-awareness is a tough skill to learn. It’s got to be even tougher to learn when you’ve had everything handed to you. Thanks for stopping by, my friend. Hope Milwaukee’s being kind to you.

Will Groovypaloosa be a family friendly affair? I hope so, because we can’t afford a babysitter for all five kids.

Yes, yes, and yes – tracking our finances has made a huge difference in our money intelligence. Watching the numbers change for the better provides excellent motivation for continuing to make changes in spending and saving.

I like your very simple method for evaluating success or failure. The key, as you pointed out, is really just being honest with yourself. Understanding the causes of unavoidable setbacks is helpful – making excuses for your poor choices is not.

Haha! Of course, Groovypaloosa will be a family friendly event. We’ll even have special entertainment for twins. And I love how tracking your key financial numbers proved to be so beneficial. Mrs. Groovy and I discovered the same thing. What’s the old saying, “You manage what you measure?” Thanks for stopping by, Harmony. You always bring a smile to my face. Hope the twins aren’t being too devilish. Cheers.

I like the no-excuses approach. For example, generations of my family have relied on welfare to survive. My parents decided that was BS, so they developed their own financial culture, went to college, and got high-paying and in-demand jobs. As a result, my sister and I got fantastic educations and broke the welfare cycle. Change is possible, but it isn’t easy.

Exactly! Thank you, Mrs. PP. We need to point out stories like yours, not to be cruel to those struggling, but to help them realize the power they have to change things. I remember a young lady in my office who moved from Buffalo to Charlotte. When I asked her why she moved, she said to get away from her family. If she stayed in Buffalo, her family’s dysfunction would have ruined her life. But because she moved away from them and adopted a new financial culture, she was able to build a pretty secure financial and personal life for herself. Ah, the power of financial redemption.

Mr G, great post, here’s hope that the morons read it! Congrats on a great trend in your first few months of retirement, I hope you’re springing for that Groovypaloosa at the end of the year (I’d offer, but I need to avoid becoming a moron).

Haha! Thanks, Fritz. Yep, I’m definitely springing for Groovypaloosa. And don’t worry, you’ll be getting the first invitation.

Hey, can we get the second 🙂

Absolutely!