This post may contain affiliate links. Please read our disclosure for more information.

Note. The title of this post was changed from Two Awesome Benefits of Being Income Poor But Asset Rich to One and a Half Awesome Benefits of Being Income Poor But Asset Rich on 6/5/2016. This was done because Brad over at Maximize Your Money found a serious error in my second supposed benefit. Correcting that error didn’t render that benefit completely meaningless. The benefit still exists, but in a much more constrained form. It’s now only a partial benefit, hence the change of the post title to One and A Half Awesome Benefits.

More than anything else, I want to provide my readers with accurate information. Getting it right is more important than protecting my ego. So my sincere thanks go out to Brad for discovering this error. He made this a better post, and he made me a better blogger.

♠ ♣ ♥ ♦

When Mrs. Groovy and I retire this October, our household income will take a dramatic hit. We’ll go from earning more than 85 percent of American households to earning less than 65 percent of American households. Ouch!

But don’t shed a tear for Mrs. Groovy and me. We have saved over 25 times our annual household expenses. So we should be able to muddle through. And, besides, the federal government has bestowed upon us—and everyone else in our income class—two awesome benefits. Here they are.

Free Healthcare

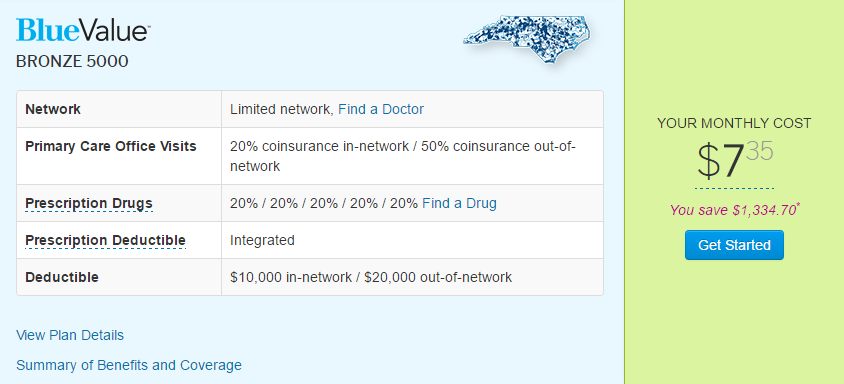

When Mrs. Groovy and I retire, our annual income will consist of a $19,100 pension and around $15,000 in dividends. From this $34,100 total, we will put $8,700 into our health saving accounts (HSAs). This will give us an adjusted gross income (for Obamacare purposes) of $25,400.

According to the BlueCross BlueShield of North Carolina website, having an adjusted gross income of $25,400 entitles us to a monthly healthcare subsidy of $1,334.70. So thanks to Obamacare, and our low income, we will pay about $100 a year for health insurance.

Political Crap (skip this if you’re not in the mood for one of my rants)

Should someone with my net worth be given a taxpayer subsidy of $16,016.40? Hell no! But I’m going to take this subsidy and here’s why. I’m a vigorous opponent of Obamacare. I believe that price transparency and competition between doctors and hospitals would do more to fix our healthcare woes than increased statism. But the political majority thinks otherwise. It fought for more government and it won. How it won its victory, in turn, also leaves me cross. The political majority did its level best to vilify me and anyone else who opposed Obamacare. We weren’t against Obamacare because we were misguided; we were against Obamacare because we were rotten people. In my mind, then, taking Obamacare subsidies is a legitimate form of protest. You can’t eff with my freedom and malign my character, and then expect me to pay for your overreach when I don’t have to. In the immortal words of a great American freedom fighter, “Homey don’t play that.”

Zero Capital Gains Tax Zero Capital Gains Tax if Your in the 15% Tax Bracket

For those in the 10 and 15 percent tax bracket, your federal long-term capital gains tax is zero. But this zero tax rate only applies to the portion of your capital gain that, when added to your adjusted gross income (AGI), is within the upper limit of the 15 percent tax bracket. For the 2016 tax year, the 15 percent tax bracket will top out at $75,300. Mrs. Groovy and I will easily be under this threshold once retired. Now, to give you an idea of how awesome this benefit might prove to be for Mrs. Groovy and me, consider the following.

In 2012, Mrs. Groovy and I began to buy stock in a company called Western Lithium (WLCDF). This company owns rights to a large lithium deposit in Nevada, just down the road from Tesla’s gigafactory.

When we first purchased WLCDF stock, its share price was $0.17. So we bought a lot of shares. And we kept on buying shares of WLCDF as its price rose to thirty, forty, and fifty cents. Today, we have 71,800 shares of WLCDF. Our total investment in the company is a little over $20K.

Now, the odds are that nothing will come of this stock (it’s currently trading at $0.39 $0.62). But let’s suppose the stars align over the next few years. Sales of the Tesla 3 take off. The gigafactory starts humming along and develops a voracious appetite for lithium. Western Lithium builds a functioning mining operation and becomes a major supplier of battery-grade lithium to Tesla. Given these favorable circumstances, it’s not inconceivable that the WLCDF share price would skyrocket, perhaps going as high as $10. And if this scenario miraculously did transpire, here are what the tax ramifications would be if Mrs. Groovy and I unloaded our stake. Note: the below deductions, exemptions, and tax rates are based on the 2016 tax year.

- Capital Gain: $698,000 ($718,000 – $20,000)

- Federal Tax: $116,261

- AGI: $10,600 ($40K income – $12.6K standard deduction – $8.1K personal exemption – $8.7K HSA contributions)

- First Capital Gains Tax: $0.00 (0% of $64,700)

- Second Capital Gains Tax: $58,748 (15% of $391,650)

- Third Capital Gains Tax: $48,330 (20% of $241,650)

- Medicare Surtax: $9,183 (3.8% of $241,650)

- State Tax: $40,135 (NC has a 5.75 flat tax)

- Free and Clear: $541,604 (This amounts to an effective capital gains tax rate of 22.4%.)

Final Thoughts

Okay, groovy freedomists, is financial independence great or what? Once you achieve it, the federal government christens you an honorary one percenter. It gives you money you don’t need (Obamacare subsidies), and it taxes you less than Warren Buffett’s secretary (at least when it comes to capital gains). That’s pretty freakin’ groovy in my book. Own your time, work when it suits you, and be treated like a one percenter. If that doesn’t inspire you to pursue FIRE with gusto, I don’t know what will.

Leave a Reply