This post may contain affiliate links. Please read our disclosure for more information.

Come the end of this year, Mrs. Groovy and I will join the ranks of the early retired. This means we’ll enter 2017 without employer-provided health insurance. For the first time in decades, we’ll be responsible for protecting our assets from the ravenous jaws of the healthcare industry. Hello Obamacare.

The nice thing about Obamacare subsidies is that they are based on income, not wealth. The less you earn, providing you remain above the Medicaid eligibility threshold, the more substantial your subsidy.

Once Mrs. Groovy and I retire, we’ll be income poor and entitled to an Obamacare subsidy. How large will that subsidy be? Here’s the calculation.

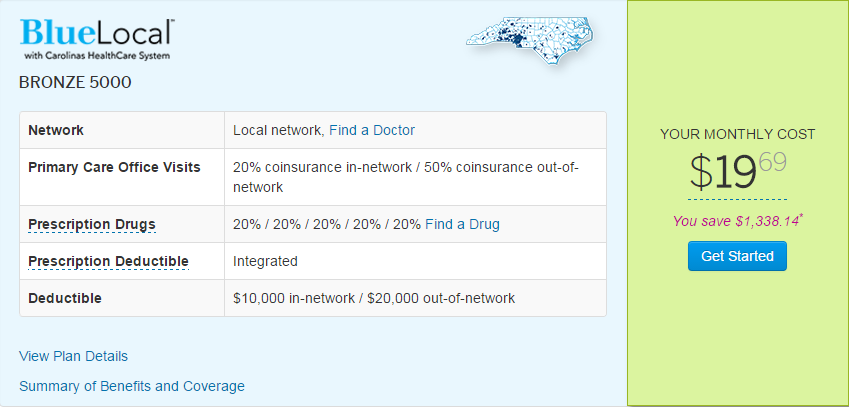

Between my pension and dividends from our brokerage accounts, our income for 2017 will be around $33K. But any money you contribute to a health savings account (HSA) is subtracted from your income for Obamacare purposes. Mrs. Groovy and I are big fans of HSAs and plan on contributing $4K each to our HSAs in 2017. This will bring our Obamacare income down to $25K. I then plugged this number into the subsidy calculator provided by Blue Cross Blue Shield of North Carolina, my state’s largest healthcare insurer. The results were shocking.

For the cheapest, high-deductible HSA eligible plan in 2016, Mrs. Groovy and I would be entitled to a monthly subsidy of $1,388. That’s over $16K for the year. And remember, this is the subsidy for 2016. The subsidy in 2017 will likely be larger.

Now, maybe I’m insane, but this bothers me. The taxpayers, many of whom can barely handle an unexpected expense of $400, will be giving Mrs. Groovy and me more than $16K. We, on the other hand, will be contributing, via property and income taxes, maybe $4K to the public good. This will make us net-takers to the tune of over $12K.

Is this right? Shouldn’t Obamacare subsidies also be based on one’s wealth? Or am I over thinking this? Mrs. Groovy certainly thinks so. She feels we have no choice but to take advantage of a system that is being shoved down our throats. For now, though, I can’t look at that net subsidy of over $12K and not think of myself as a soon-to-be teat-sucking layabout.

What are your thoughts?

Leave a Reply