This post may contain affiliate links. Please read our disclosure for more information.

Earlier this year, I started looking into Obamacare. I wanted to get an idea of what health insurance would cost me in 2017, the first calendar year Mrs. Groovy and I would be retired and would thus no longer have employer-provided health insurance. Here is what I found on the Blue Cross Blue Shield website.

Estimated income: $33,000 (Pension plus dividends)

Estimated Obamacare income: $25,000 (Estimated income less $8,000 for Health Savings Accounts)

Annual premium: $236.28

Annual Obamacare subsidy: $16,057.68

Deductible: $10,000

Now remember, the above numbers come from my analysis done in January. So they reflect 2016 premiums and subsidies. Actual 2017 premiums and subsides turned out to be much higher. Also, we decided to forego plans with a Health Savings Account (HSA). Mrs. Groovy has ice in her veins when it comes to investing. But when it comes to healthcare, she’s a wuss. She also agrees with Maarten over at MillionIn10 that insurance money shouldn’t be used as an investment. And since she’s the Supreme Allied Commander of the Groovy household, we’re NOT going with an HSA-eligible Bronze plan. A $13,000 deductible scares the crap out of her (yes, the deductible for the Bronze plan went up as well). We’re going with a Silver plan instead. Here, then, are our real Obamacare numbers for 2017.

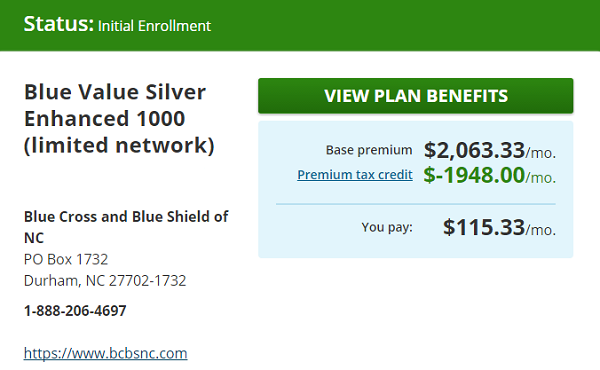

Estimated income: $30,000 (Pension plus dividends)

Estimated Obamacare income: $30,000 (Buh-bye Health Savings Accounts)

Annual premium: $1,383.96

Annual Obamacare subsidy: $23,376

Deductible: $2,000

If you noticed, the estimated income for 2017 that I punched into HealthCare.gov is $3,000 less than I calculated back in January. Mrs. Groovy pointed out that we could reduce our Obamacare expenses even more by arranging our income to fall between 150-200% of the Federal Poverty Level (FPL). (For a good post on this check out Justin over at the Root of Good.) Incomes in this range are eligible for cost-sharing subsidies that reduce co-pays, deductibles, and out-of-pocket maximums. For a household of two people, 200% of the 2017 FPL is $32,040. Manipulating our dividend income to produce an income of $30,000 is thus a tad excessive. But I’m not going to argue with Mrs. Groovy. If the Supreme Allied Commander wants a 2017 income of $30K, I’ll invest as much as necessary in 3-month T-bills to make it happen.

Thoughts on Obamacare

Ethics

You’re not obligated to ignore tax loopholes that reduce your tax burden. If the federal government says you can deduct local taxes and mortgage interest from your gross income, and thus reduce the amount of your income subject to federal taxes, you’re not greedy or unpatriotic if you choose to take advantage of this. In fact, if you’re a homeowner in a state with high taxes and expensive housing (e.g., California, Massachusetts, New York, etc.), you’d be foolish not to take advantage of these loopholes. Likewise, you’re not obligated to ignore subsidies that increase your purchasing power. If the federal government wants to pay for all or most of your health insurance costs, and thus free you to spend more of your money on other wants, you’re not a teat-sucking layabout or a parasite if you choose to accept this gift.

And, yet, I still feel crappy about my Obamacare subsidies. Philosophically, I’m opposed to subsidies for the rich and middle-class. I don’t think the taxpayers should be handing me a gift of over $23K—especially since a good chunk of them can’t come up with $400 to cover an emergency. But as I explained in an earlier post, I’m going to take the subsidies. It’s my way of saying F-YOU to our elites. In lobbying for Obamacare, they maligned my character. In passing Obamacare, they degraded my freedom (e.g., making catastrophic plans illegal and forcing me to buy maternity coverage). So why should I ignore Obamacare subsidies and pay for their callous overreach myself? Yes, I feel crappy about it (is that Mr. Hypocrisy gnawing at my conscience?), but I just can’t bring myself to be that self-loathing.

Something’s Rotten in ACA-Land

In one sense, Obamacare is working. I and millions of other Americans, because of very generous subsidies, are getting free or low-cost health insurance. Great! But what about the people who are paying for those generous subsidies? Is Obamacare working for them?

Judging whether a government program is working by only looking at those who receive the program’s benefits is not exactly honest. Imagine if Gallup existed in the antebellum South and it decided to see if slavery was working by only polling the plantation owners?

When I look at all sides of the Obamacare equation, I don’t see success. I see failure. First, the obligated—those taxpayers who pay for Obamacare’s generous subsidies—don’t have any protections. The entitled—those who get Obamacare subsidies—have an unlimited right to the obligated’s income. If doctors, hospitals, big pharma, and insurance companies need more money to make healthcare happen for the entitled—fine, no problem. Just send the adjusted bill to the obligated (i.e., the schmuck taxpayers). Second, Obamacare sets a precedent that doesn’t bode well for freedom. If the federal government can force you to buy health insurance, why can’t it force you to buy life insurance, disability insurance, or extended warranties? Sure, this sounds rather far-fetched. But you know what also seemed rather far-fetched until very recently? President Trump. Finally, third, Obamacare hasn’t done diddly squat to bend the cost curve in a favorable direction. It would be one thing if deductibles and premiums were going down—or even staying flat. But they’re not. Every year they’re going up, often dramatically. The average Obamacare premium went up 25% for 2017 policies. In 8 states, Obamacare premiums went up more than 30%. Here are the scary numbers.

- Alabama: 36%

- Georgia: 32%

- Illinois: 44%

- Minnesota: 50-67%

- Nebraska: 35%

- Oklahoma: 76%

- Pennsylvania: 33%

- Tennessee: 44-62%

Keep the One Good Thing About Obamacare

I’m just a little ol’ country blogger, and no one in the Trump administration or Congress gives a rat’s ass what I think. But if the Republicans do decide to repeal and replace Obamacare, their new plan needs to provide for those with pre-existing conditions. Just because the fickle finger of fate has frowned upon you and made you medically uninsurable doesn’t mean you should be resigned to a life of sickness and pauperism.

One simple solution to this problem is Medicare. Right now Medicare covers those who are uninsurable because of their age. Create Medicare Part P (P for pre-existing) and cover those who are under 65, have an income, and are uninsurable because of a pre-existing condition. And base the cost of the Part P premium on the severity of the pre-existing condition. Those with more medically taxing conditions should pay higher premiums. Part P premiums, however, shouldn’t cost more than 10-15% of a person’s income.

And what about those with pre-existing conditions who are under 65 and poor? Medicaid—if they aren’t eligible for it already.

Bend the Cost Curve in the Right Direction

Insurance is expensive because healthcare is expensive. It’s not because healthcare providers are charging $200 for an MRI and insurers are paying them $2,000. In fact, it’s the exact opposite. Insurers never pay the sticker price. If insurers did pay sticker prices, the cost of health insurance would be even more ridiculous. Here, then, are some ways to make healthcare truly affordable. I hope the Republicans are listening.

- Let health insurance be insurance. You get insurance to protect your wealth from unusual expenses. Think car insurance. You don’t get car insurance to pay for fill-ups and oil changes. You get it to pay for major accidents. Likewise, most healthy Americans can pay for routine healthcare out of pocket. They only need insurance for the big stuff (cancer, by-pass surgery, hip replacement, etc.). So don’t force Americans to pay for more coverage than they need; don’t make catastrophic health insurance illegal.

- Require doctors and hospitals to disclose their prices. Price transparency and competition is the best way to reduce healthcare costs.

- End price discrimination. Why is it okay for a hospital to charge an insured patient $1,000 for a procedure but then charge an uninsured patient $5,000 for the same procedure?

- Let patients decide how much damage they can sue for. If they merely want a surgeon to fix any screw up he or she might make, then the surgery will cost X. If they want to be able to sue for unlimited damages, then the surgery will cost 10X.

- Reform our licensing laws so nurses and physician assistants can provide more healthcare. There’s no reason why nurses can’t stitch up minor lacerations, and there’s no reason why physician assistants can’t perform minor surgeries.

- Encourage insurers to take advantage of medical tourism. It doesn’t make any sense for Medicaid to pay $30,000 for a hip replacement in San Diego when a competent surgeon in Tijuana can do it for $10,000.

Final Thoughts

I prefer freedom to Leviathan. Free people are more apt to fix things than politicians and lobbyists. But maybe I’m nuts. Maybe government managed healthcare is the way to go. What say you? Should the Republicans try to repeal and replace Obamacare? Or should the Republicans just leave things alone? Let me know what you think when you get a chance. Peace.

The question I don’t hear often enough is: “why does every other economically advanced Western democracy provide universal coverage?”

The follow-up is: “how is it working in those countries?” Really working, not the horror story anecdotes from the past that are always trotted out – but in actual healthcare metrics like life expectancy, infant mortality, cancer survival rates, etc.

And the last follow-up is why is no one really considering a baseline medicare for all coverage model? A here’s the basics sort of plan and if you want more you can buy it on the open market sort of plan?

Healthcare is unlike most other markets in that you the patient, and a partial payer in an HSA model, are not the person who can even see prices most of the time, you have no ability (or limited ability) to negotiate rates and often (in the event of a major illness or accident) are not in position to negotiate (unconscious, etc). Much of healthcare isn’t elective in nature (nose jobs, etc) – and while you can choose not to go to the ER for a cold, you most likely aren’t going to wait if you’ve had a stroke or an accident. Also healthcare is the rare product or service that almost every single person eventually needs.

I know my FI calculations dramatically improve once I turn 65 and will have Medicare as a baseline. Thankfully I will not be eligible for Medicaid (unless something dramatic happens) so I’ll be paying for plans on the open market once I leave my employer. The gray area is between then and when I turn 65 (which also thankfully is a ways away). I think far too many people in the FI community neglect and negate the need for healthcare coverage once they leave the employer provided coverage behind. Being healthy and 40 or 45 is very different from being healthy and 55 or 60. While I trust my portfolio to cover my expenses with room to spare and room from growth, I have no of knowing what might happen with my health, and healthcare costs.

This is an interesting and fair assessment of the ACA or Obamacare since you get into the realities of being an individual with needs compared to an individual with political philosophies. I am curious about what your opinion is of it now after being on it and using it vs. all of the rhetoric on both sides about what they said it would be.

Hey, Kevin. Mrs. Groovy and I went for our wellness exams a few weeks ago. We didn’t have any out-of-pocket costs for these services because they are part of the mandatory benefits. If this turns out to be a typical year, I won’t see a doctor again. So the taxpayers and I will end up paying over $12K (half the total premium for my household of two people) for an exam that would probably cost around $200 in a competitive environment. I get that the taxpayers and I are paying for insurance and the premiums are large because unexpected medical bills could be very large. But I also get the concept of over insurance. If I were the Supreme Ruler of the United States, I would allow people to insure their health the way they insurance their cars. People have car insurance to protect their cars and other assets from major accidents. They don’t have car insurance to pay for fill ups, oil changes, inspections, and repairs. Likewise, I would prefer health insurance that covered major illnesses like cancer and heart attacks. I can handle wellness exams and minor ailments. Ninety percent of our healthcare issues would be fixed by HSAs, price transparency, greater competition, and catastrophic healthcare insurance. Those who are uninsurable or have chronic ailments should be placed on Medicare. Sorry for the rant, Kevin. But those are my impressions three months into Obamacare. Thanks for stopping by, my friend. I really appreciate it.

Thanks for the input and the rant is OK. I can’t say I disagree with what you presented and I have similar thoughts but I get my healthcare through my employer. I wish healthcare wasn’t tied to employment which adds a whole other level of complication for both the individuals and companies. So much is not transparent and frankly both parties are using it as a way to get more votes rather than just solve the issue, assuming they even know how to.

I don’t qualify for a subsidy, but I am really happy with how the ACA has impacted my life. I pay a reasonable price each month that went up a small amount this year. My co-pays are high, but I am healthy. This is possible because of how my state decided to implement their exchange. Or perhaps I’m a unicorn and somehow slipped through the health insurance cracks, but I think it’s probably living in a liberal state that wanted ACA to succeed and did what it could to make ACA work properly with or without the help of the insurance industry.

The ACA definitely did some good things. But my biggest gripe against it is that it does nothing to reduce the cost of healthcare. It reduces the cost of health insurance for millions, but not the cost of healthcare. Case in point. Two years ago, during my annual wellness exam, the PA noticed my ears had a lot of wax build-up and suggested a cleaning. So even though I would be paying for the cleaning out of pocket (I had high-deductible policy with an HSA), I said sure without asking what it would cost. Big mistake. That cleaning cost me $125! For a tech to take five minutes and clean out my ears with a big syringe! What would this cleaning have cost in Mexico? Five dollars? I’ll never agree to any healthcare again without first asking about costs. What our healthcare system needs is price transparency and incentives for patients to seek out the lowest-cost hospitals and doctors. And the ACA fails miserably in this regard. If only our politicians can craft a system that fuses the best parts of the ACA with the best parts of free market capitalism. It will never happen, of course. But one can dream. Thanks for stopping by, ZJ. It’s always great hearing from you.

Back in 2007, I looked into a catastrophic plan for myself. It was around $100 month with a $2,500 deductible. I’m ten years older now (55 vs. 45), but I don’t imagine a catastrophic plan would cost me much more–especially since I could comfortably increase the deductible to $5,000 or $10,000. And imagine what a catastrophic plan would cost if there were price transparency and competition! A little freedom and a little market discipline would go a long way toward improving our healthcare system. But Democrats and Republicans love controlling things. This way they can pound their chests and proclaim to the electorate how important they are to life on earth. Controlling things is also a great way to extract tribute from the wealthy. Meh. Hopefully Trump and the Rs and Ds can make healthcare a little less dicey for those in the FIRE community. I got my fingers crossed, MSM. I’m ten years shy of Medicare. Cheers, my friend.

I have to say that the thing that scares me the most when it comes to FIRE is health insurance.

I’m hoping that health insurance remains affordable and with a couple of small tweaks that it can keep the majority of US citizens happy and healthy.

Hopefully the Republicans and Democrats will agree on more than they did in the Obama administration and work on things that need to be fixed.

Hey Mr G, how’s it going? I’m not from the US, so I don’t really know much about Obamacare. The only thing I feel the government should do, is to make sure that healthcare is affordable for everyone. The lower income should get more subsidies and the higher income should pay their fair share. There shouldn’t be two different prices on the same procedure.

Hopefully President Trump can point healthcare to the right direction!

Thanks, TTW. You summed it up very well. It shouldn’t be nearly as complicated as we’ve made it. Expose medical costs, encourage patients and insurers to shop for the best prices, and subsidize the poor. Easy-peasy. Hopefully Trump will improve our “hot mess” healthcare system. I’m not counting on it, but I got my fingers crossed.

There’s nothing that scares me more about our early retirement than how we’re going to manage health care insurance (we’ll have a 10 year bridge, since we’ll retire at Age 55). I expect we’ll see continued modifications to the system, and continued cost increases. Scary stuff, this.

C’mon, Fritz. You’re made of sterner stuff than that. Fear not our “hot mess” healthcare system. Just start the DIY surgery movement. I’m sure with a manual, YouTube, and Mrs. TRM’s help, you can handle your own angioplasty. Not only will it be a great experience, it will make for a great frugality post on your blog.

In all seriousness, my friend, I’m just as scared about our “10 year bridge” as you are. Thanks for stopping by.

I completely agree with so much of what you’ve said here! I wrote my piece on the matter on Monday and my wishlist is pretty similar. You shouldn’t feel bad one bit about getting the subsidy…I can’t help but think of “don’t hate the player, hate the game”. You’re just playing by their rules, no crime no foul.

I agree on pre-existing conditions. Everyone with a hearty and any common sense should agree with that.

There are a lot of tweaks Trump and the republicans can and hopefully will make to the system, but no need for a complete repeal and replace and I think they will back off that.

Great post!

Thanks, TGS. Something certainly has to give. Obamacare got some things right but didn’t come close to getting healthcare costs under control. Let’s hope Trumpcare does a better job. I’m not taking any chances, though. Mrs. G and I will continue learning as much as we can about medical tourism. If things get worse here, there’s always India, Singapore, or Thailand. Just think about it! The fusing of world travel and healthcare. You can have triple-bypass surgery in Bangkok and recuperate in Chiang Mai. What could go wrong? Cheers, my friend.

This is a very thought provoking article, Mr. G. And I agree on some, and have questions about others.

First, to your point about medical insurance not really being insurance…I’ve said that for years. What other form of insurance do you EXPECT to use each year? None. Insurance is for catastrophic events, so health insurance isn’t really insurance at all unless you do have catastrophic coverage. If catastrophic-only coverage was the norm, you better believe costs would come down, but it works far less because there’s so many other options.

And YES to price transparency, non-price discrimination (geez, talk about a ridiculous system), and probably more nurse-led care.

But the lawyer’s kid in me looks at this statement “If they merely want a surgeon to fix any screw up he or she might make, then the surgery will cost X” and says “But what if the screw up causes permanent damage requiring permanent care or restricting ability to work? This assumes the damage is repairable, and that’s not necessarily true with the human body.”

And I’m highly afraid of “Repeal and Replace,” because it sounds an awful lot like “Repeal and screw everyone who can’t afford care.” Congress refused to do things that would have made ACA work the way they talked about. Now they are discussing doing away with Medicare altogether, leaving millions of folks in untenable situations as they age and need more care. Even if none of it affects anyone currently getting Medicare, I don’t relish the thought of “Freedom FROM Medicare and Social Security” in my future.

ACA tried to fix an untenable situation of ridiculously rising health care costs. It worked for some (early retirees, uninsured, lower income folks, folks with preexisting conditions, 20-25 year olds whose parents could insure them) and made things worse for others (people who pay for their own health insurance with little to no subsidies, people who don’t want to be insured or only need catastrophic coverage.)

All policies seem to have winners and losers. But is NO healthcare for millions of Americans really an option that our country wants to live with? (and being in NC, you know there are all kinds of folks that don’t qualify for Medicare or the subsidies and just don’t get care.) It kinda just sounds like Freedom to suffer.

Haha! I love the lawyer’s kid in you. Mrs. Groovy said the same thing about patients deciding how much damage they want to sue for. What happens if a surgeon removes the wrong leg? So, yes, my suggestion to reduce healthcare costs by modifying our malpractice laws probably isn’t feasible. But something’s got to give. Medicare-for-all (i.e., universal coverage) won’t stop rising healthcare costs. Healthcare costs will continue to grow and will eventually start crowding out spending on the other wants such as defense, education, and housing. It happened in Europe and it will happen here. And for what? Making health insurance more like insurance will not end healthcare. Auto insurance that only covers accidents doesn’t stop car care. Americans will just pay for most of their healthcare like they do other things (i.e., comparing price and quality and seeking out the best provider given their circumstances). And healthcare providers will just have to adjust to the new reality (i.e, competition). Provider A won’t be able to charge $12K for a broken elbow if 1) there’s no Cigna or Medicare to bill, and 2) Providers B, C, and D are willing to fix broken elbows for far less. When I was born in 1961, it cost my uninsured parents $150–and my mom was in the hospital for three days. My dad was making around $60 a week at the time and he paid the doctor $10 month until it the bill was paid in full. Why was healthcare more affordable back then when Americans, in general, were significantly poorer than today? I certainly don’t have the answers. But the lack of price transparency and competition can’t be helping matters. And health insurance that pays for everything from ear cleanings to brain surgery is a major obstacle to price transparency and competition. Thanks for stopping by, Emily. Your comment was as spot on and thought-provoking as ever. I really appreciate that you challenged my ideas. It made me realize I have more thinking to do.

While I don’t think the ACA is a complete success, I do want to address a couple things. “Obamacare hasn’t done diddly squat to bend the cost curve in a favorable direction” isn’t exactly true. According to http://www.factcheck.org/2015/02/slower-premium-growth-under-obama/, premiums have grown more slowly under Obama’s tenure. That isn’t exactly a reduction in premiums, but it is an improvement despite how it may appear. And while “most healthy Americans can pay for routine healthcare out of pocket”, that seems to ignore the vast numbers of people who have chronic conditions. Not cancer or hip surgery, but conditions like mine (congestive heart failure and diabetes) that require a moderate to significant cost outlay on a regular basis (especially when it comes to prescription medicines).

I do think the ACA has been beneficial in getting more Americans insured and insuring those with pre-existing conditions, and as ChooseBetterLife mentioned, removing the lifetime cap. I hope whatever changes (or replacements) are made, that those benefits remain. Personally, my wife and I are on Medicare which has worked pretty well for us. I just hope that it won’t be cut or replaced under the new administration.

I hope you’re right about premium growth under Obamacare. My fear is that the lower growth is only the result of more Americans being on high-deductible plans. How common have high-deductible plans become? I don’t have the answer. I’ll have to research it. All I know is that high-deductible plans were practically unheard of ten years ago and now they’re very commonplace. And excellent point about chronic conditions. I assumed that was the equivalent of a pre-existing condition. So, yes, people with health maladies that make them uninsurable or saddle them with monstrous bills should be on Medicare Part P. Damn this healthcare stuff is hard! Thanks for stopping by, Gary. You made me a little more knowledgeable.

Thanks for the mention my good Groovy people!

I have mixed feelings about the equity with the ACA. On the one hand, it helps tens of millions access health insurance that they couldn’t get before. On the other hand it’s done nothing to reduce healthcare expenditures or costs overall, and in fact probably increases medical costs due to increased demand (“throw money into a market to stimulate demand and the price goes up”).

I’m not sure how to wake us up from this national healthcare nightmare. Single payer? A basic “free”/cheap health plan for everyone with premium supplemental policies (think Medicare + supplemental plans)? Private insurance with a reinsurance company taking on risk from insurers who underwrite those with pre-existing conditions?

One thing is certain – there’s currently a massive bloat of overhead with the current set up with insurance companies and billing departments. What if we shifted those funds from white collar positions to white coat positions? Might be magic.

I was just about to weigh in on the excessive bloat with billing and insurance overheads but Justin beat me to it. In my opinion, this is where there needs to be a complete overhaul. Today we are seeing Tesla and Google design driverless cars. And we can’t friggin clean up the healthcare admin nightmare that is sucking the system dry. It’s nonsense, absolute nonsense that this can’t be addressed.

Having worked in big pharma for nearly 25 years, I know how hard it is to discover safe and efficacious new drugs. It is simply brutal. I work with such talented scientists and even the sharpest minds working together find it hard to crack devastating diseases like Alzheimer’s, Blood cancers, Crohn’ s disease. But try we must. And trying relentlessly ain’t cheap. Yes, there are some practices that pharma can do much better at such as lobbying and marketing techniques.

We will be in the MAGI zone where we are unlikely to get much subsidy with Obamacare/Trumpcare/Nobloodycares . I have the option to go with my employer plan when we hit FIRE in less than 2 years. It may be slightly higher than a silver plated plan on the exchange but likely less sensitive to cost increases over time judging by the last few years. Can’t say I am thrilled with all the uncertainty. Something has to give. The taxpayer.

You never fail to bring a smile to my face, Mr. PIE. “Obamacare/Trumpcare/Nobloodycares”–that, my friend, is priceless. As Julie so aptly pointed out, healthcare in the US is a “hot mess.” So many things need to be fixed, you don’t know where to begin. You are so right about excessive bloat when it comes to overhead. But this is largely the result of insurance paying for everything from ear cleanings to brain surgery. Imagine how much bloat there would be in car insurance overhead if car insurance paid for fill-ups and oil changes! Maybe we’re asking insurance to do too much in the healthcare field?

I like where you’re going, Justin: Basic insurance that covers large, unexpected medical expenses; medi-stamps (i.e., the healthcare equivalent of food stamps) for those with pre-existing conditions; and price transparency and competition to hold down costs and reduce overhead. Not a perfect solution, but certainly better than the status quo. More government control hasn’t been working. All we’re getting is a double-whammy. More dependency and more costly healthcare.

Thank you for the mention. You are getting some awesome credits. For our family of 4 we’re still paying close to $600 a month after credits. In our scenario I actually have to make an income of $65,000 to have all of us eligible.

Not inflating our income and reducing our credits, would put our kids in CHIP (I believe similar to Medicaid). In CHIP we would not get the medical equipment covered, needed for our son’s medical condition. The out of pocket cost would outweigh the additional premium.

I agree things are broken in ObamaCare land. The idea of universal coverage is noble (and standard in any other western nation) but was lost with the medicaid gap. There are still millions left uninsured because of it.

The cost of medical care and pharmaceutical cost are the next broken. These are no longer market forces at work but pure unadulterated greed. If a government takes to step to mandate insurance for all, it should also have the balls to stand up against out of control corporations and their pricing practices. Costs that are currently all passed on to the american people.

BTW, for some reason cost of ACA remained the same for 2017 in Wisconsin. I was “pleasantly” surprised by the lack of a huge cost increase next year.

Hey, Maarten. I truly think that price transparency and competition are the only things that can curb our ridiculous healthcare costs. Universal coverage may blunt annual increases, but I don’t see how that will stop pharmaceuticals, hospitals, and healthcare professionals from lobbying Congress and manipulating the system for their benefit. I hope I’m not being too cynical. I just see healthcare going the way of education. More government control, more taxes, and no improvement–with the same dreary excuses year after year after year. Meh. But on a happier note, it’s nice to see that the insurers in your state gave you a break this year on the premium increases. Perhaps there is hope. Thanks for stopping by, Maarten. I truly appreciate your contributions to the conversation.

So many good points here. I agree completely that pre-existing conditions should be covered. The ACA also removed the lifetime cap from some plans, which was often $1Million. Chemotherapy, an organ transplant, injuries from a major car accident, and other fairly common treatments can break through that limit quite easily.

Other thoughts should include improving malpractice laws, which is one reason that nurses and PAs don’t do many procedures. Why would they want the liability of missing a tendon laceration or a foreign body when suturing a laceration? Better to leave the risk to the docs, so we don’t all have to pay the malpractice premiums and suffer the worry and ulcers while doing our best.

Another fact that many people don’t know is that the government has an unfunded mandate called EMTALA. It guarantees Emergency Department evaluation and treatment for everyone, regardless of the ability to pay. It’s one of the reasons I chose this specialty because I didn’t want to turn away people who couldn’t pay.

However, hospitals, nurses, docs, techs, etc. work very hard and 25-40% of our patients used to be uninsured (and many still are), so we never collected a dime. Many who now have HSA plans still don’t pay a dime of their large deductibles.

Another huge percentage of patients is on Medicaid, which pays less than our costs, so we lose money on all of those patients too. Medicare usually pays about what it costs to treat, so we barely break even most of the time.

The system is a hot mess, and it’s more complicated than most people realize.

Hey, Julie. Thanks for jumping in. I have much to learn and it’s great that someone on the front lines has stopped by to help. Excellent points. I totally forgot about the ACA provision that eliminates life-time caps. If Obamacare is repealed and replaced, I hope they retain that feature. Got a question for you. Are emergency rooms set up for possible cash/credit card payments? It seems to me that a lot of people use emergency room care for non-emergencies. They may not have health insurance, but many of them surely have cash and/or credit cards. Can emergency rooms charge them at least for the visit, say $100?

President Trump has already said that he prefers to keep provisions of pre existing conditions. I think Repeal and Replace is off the table. I don’t know, call it pick and choose. They seem to want consumers to be able to shop across state lines which may dramatically lower costs as well. It’s an exciting time that’s for sure!

We’ll see. I agree that “repeal and replace” is probably off the table. The Republicans talk a good game but are lousy at follow through. I guess we’ll just be stuck with $100K college degrees, $500K cancer treatments, and billion dollar fighter jets until the world doesn’t want to lend us money anymore. Like you said, Go4, “exciting times.” Thanks for stopping by, my friend.