This post may contain affiliate links. Please read our disclosure for more information.

Earlier this year, I started looking into Obamacare. I wanted to get an idea of what health insurance would cost me in 2017, the first calendar year Mrs. Groovy and I would be retired and would thus no longer have employer-provided health insurance. Here is what I found on the Blue Cross Blue Shield website.

Estimated income: $33,000 (Pension plus dividends)

Estimated Obamacare income: $25,000 (Estimated income less $8,000 for Health Savings Accounts)

Annual premium: $236.28

Annual Obamacare subsidy: $16,057.68

Deductible: $10,000

Now remember, the above numbers come from my analysis done in January. So they reflect 2016 premiums and subsidies. Actual 2017 premiums and subsides turned out to be much higher. Also, we decided to forego plans with a Health Savings Account (HSA). Mrs. Groovy has ice in her veins when it comes to investing. But when it comes to healthcare, she’s a wuss. She also agrees with Maarten over at MillionIn10 that insurance money shouldn’t be used as an investment. And since she’s the Supreme Allied Commander of the Groovy household, we’re NOT going with an HSA-eligible Bronze plan. A $13,000 deductible scares the crap out of her (yes, the deductible for the Bronze plan went up as well). We’re going with a Silver plan instead. Here, then, are our real Obamacare numbers for 2017.

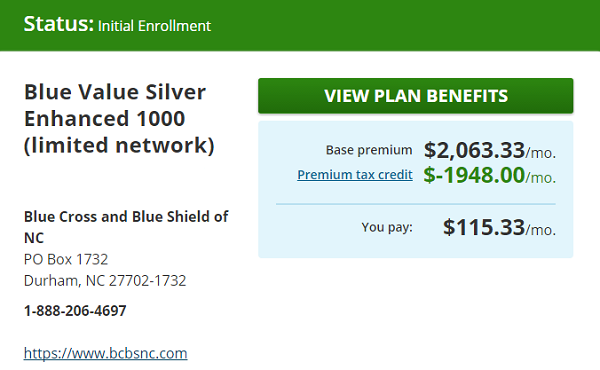

Estimated income: $30,000 (Pension plus dividends)

Estimated Obamacare income: $30,000 (Buh-bye Health Savings Accounts)

Annual premium: $1,383.96

Annual Obamacare subsidy: $23,376

Deductible: $2,000

If you noticed, the estimated income for 2017 that I punched into HealthCare.gov is $3,000 less than I calculated back in January. Mrs. Groovy pointed out that we could reduce our Obamacare expenses even more by arranging our income to fall between 150-200% of the Federal Poverty Level (FPL). (For a good post on this check out Justin over at the Root of Good.) Incomes in this range are eligible for cost-sharing subsidies that reduce co-pays, deductibles, and out-of-pocket maximums. For a household of two people, 200% of the 2017 FPL is $32,040. Manipulating our dividend income to produce an income of $30,000 is thus a tad excessive. But I’m not going to argue with Mrs. Groovy. If the Supreme Allied Commander wants a 2017 income of $30K, I’ll invest as much as necessary in 3-month T-bills to make it happen.

Thoughts on Obamacare

Ethics

You’re not obligated to ignore tax loopholes that reduce your tax burden. If the federal government says you can deduct local taxes and mortgage interest from your gross income, and thus reduce the amount of your income subject to federal taxes, you’re not greedy or unpatriotic if you choose to take advantage of this. In fact, if you’re a homeowner in a state with high taxes and expensive housing (e.g., California, Massachusetts, New York, etc.), you’d be foolish not to take advantage of these loopholes. Likewise, you’re not obligated to ignore subsidies that increase your purchasing power. If the federal government wants to pay for all or most of your health insurance costs, and thus free you to spend more of your money on other wants, you’re not a teat-sucking layabout or a parasite if you choose to accept this gift.

And, yet, I still feel crappy about my Obamacare subsidies. Philosophically, I’m opposed to subsidies for the rich and middle-class. I don’t think the taxpayers should be handing me a gift of over $23K—especially since a good chunk of them can’t come up with $400 to cover an emergency. But as I explained in an earlier post, I’m going to take the subsidies. It’s my way of saying F-YOU to our elites. In lobbying for Obamacare, they maligned my character. In passing Obamacare, they degraded my freedom (e.g., making catastrophic plans illegal and forcing me to buy maternity coverage). So why should I ignore Obamacare subsidies and pay for their callous overreach myself? Yes, I feel crappy about it (is that Mr. Hypocrisy gnawing at my conscience?), but I just can’t bring myself to be that self-loathing.

Something’s Rotten in ACA-Land

In one sense, Obamacare is working. I and millions of other Americans, because of very generous subsidies, are getting free or low-cost health insurance. Great! But what about the people who are paying for those generous subsidies? Is Obamacare working for them?

Judging whether a government program is working by only looking at those who receive the program’s benefits is not exactly honest. Imagine if Gallup existed in the antebellum South and it decided to see if slavery was working by only polling the plantation owners?

When I look at all sides of the Obamacare equation, I don’t see success. I see failure. First, the obligated—those taxpayers who pay for Obamacare’s generous subsidies—don’t have any protections. The entitled—those who get Obamacare subsidies—have an unlimited right to the obligated’s income. If doctors, hospitals, big pharma, and insurance companies need more money to make healthcare happen for the entitled—fine, no problem. Just send the adjusted bill to the obligated (i.e., the schmuck taxpayers). Second, Obamacare sets a precedent that doesn’t bode well for freedom. If the federal government can force you to buy health insurance, why can’t it force you to buy life insurance, disability insurance, or extended warranties? Sure, this sounds rather far-fetched. But you know what also seemed rather far-fetched until very recently? President Trump. Finally, third, Obamacare hasn’t done diddly squat to bend the cost curve in a favorable direction. It would be one thing if deductibles and premiums were going down—or even staying flat. But they’re not. Every year they’re going up, often dramatically. The average Obamacare premium went up 25% for 2017 policies. In 8 states, Obamacare premiums went up more than 30%. Here are the scary numbers.

- Alabama: 36%

- Georgia: 32%

- Illinois: 44%

- Minnesota: 50-67%

- Nebraska: 35%

- Oklahoma: 76%

- Pennsylvania: 33%

- Tennessee: 44-62%

Keep the One Good Thing About Obamacare

I’m just a little ol’ country blogger, and no one in the Trump administration or Congress gives a rat’s ass what I think. But if the Republicans do decide to repeal and replace Obamacare, their new plan needs to provide for those with pre-existing conditions. Just because the fickle finger of fate has frowned upon you and made you medically uninsurable doesn’t mean you should be resigned to a life of sickness and pauperism.

One simple solution to this problem is Medicare. Right now Medicare covers those who are uninsurable because of their age. Create Medicare Part P (P for pre-existing) and cover those who are under 65, have an income, and are uninsurable because of a pre-existing condition. And base the cost of the Part P premium on the severity of the pre-existing condition. Those with more medically taxing conditions should pay higher premiums. Part P premiums, however, shouldn’t cost more than 10-15% of a person’s income.

And what about those with pre-existing conditions who are under 65 and poor? Medicaid—if they aren’t eligible for it already.

Bend the Cost Curve in the Right Direction

Insurance is expensive because healthcare is expensive. It’s not because healthcare providers are charging $200 for an MRI and insurers are paying them $2,000. In fact, it’s the exact opposite. Insurers never pay the sticker price. If insurers did pay sticker prices, the cost of health insurance would be even more ridiculous. Here, then, are some ways to make healthcare truly affordable. I hope the Republicans are listening.

- Let health insurance be insurance. You get insurance to protect your wealth from unusual expenses. Think car insurance. You don’t get car insurance to pay for fill-ups and oil changes. You get it to pay for major accidents. Likewise, most healthy Americans can pay for routine healthcare out of pocket. They only need insurance for the big stuff (cancer, by-pass surgery, hip replacement, etc.). So don’t force Americans to pay for more coverage than they need; don’t make catastrophic health insurance illegal.

- Require doctors and hospitals to disclose their prices. Price transparency and competition is the best way to reduce healthcare costs.

- End price discrimination. Why is it okay for a hospital to charge an insured patient $1,000 for a procedure but then charge an uninsured patient $5,000 for the same procedure?

- Let patients decide how much damage they can sue for. If they merely want a surgeon to fix any screw up he or she might make, then the surgery will cost X. If they want to be able to sue for unlimited damages, then the surgery will cost 10X.

- Reform our licensing laws so nurses and physician assistants can provide more healthcare. There’s no reason why nurses can’t stitch up minor lacerations, and there’s no reason why physician assistants can’t perform minor surgeries.

- Encourage insurers to take advantage of medical tourism. It doesn’t make any sense for Medicaid to pay $30,000 for a hip replacement in San Diego when a competent surgeon in Tijuana can do it for $10,000.

Final Thoughts

I prefer freedom to Leviathan. Free people are more apt to fix things than politicians and lobbyists. But maybe I’m nuts. Maybe government managed healthcare is the way to go. What say you? Should the Republicans try to repeal and replace Obamacare? Or should the Republicans just leave things alone? Let me know what you think when you get a chance. Peace.

Leave a Reply to Emily @ JohnJaneDoe Cancel reply