This post may contain affiliate links. Please read our disclosure for more information.

If you’re a FIRE enthusiast, and you don’t want to be mocked and vilified by other FIRE enthusiasts, you better know the following numbers like the back of your hand.

Monthly Expenses

In order to know your FI target number—the amount of money needed to be considered financially independent—you need to know your monthly expenses. Your FI target number is based on your annual expenses which are based on your monthly expenses. Here’s the formula for your FI target number.

FI Target Number = Monthly Expenses x 12 x 25

Knowing your monthly expenses is critical for another reason. One tried and true way of increasing your savings is to reduce your spending. And how do you know where you can economize? You can’t unless you know where your money is going. So you better track your spending and become intimately familiar with what you spend every month on average. If you fail to do this, three lamentable things will happen.

- You’ll have no idea what your FI target number is.

- You won’t have the knowledge necessary to give your frugality muscles a proper workout.

- And you’ll be shunned at FinCon. No one will sit next to you at whatever breakout session you attend.

Quick aside. If you don’t have an expense-tracking spreadsheet, here’s the one I use.

Groovy Expense Tracker Groovy Expense Tracker GuideMonthly Savings

You won’t get to your FI target number by being a spendthrift. You need to save money—a lot of money. And you can’t allow all of your savings to languish in a savings account earning one percent annually. If you’re going to reach FI before you’re old and withered, your savings need to be earning seven to ten percent annually. Your savings, in other words, need to be horny little buggers who make more dollars than inflation kills.

To calculate your monthly savings, sum all the money you contribute to the following accounts during a typical month:

- Workplace retirement accounts (e.g., 401(k), 403(b), and 457(b))

- Non-workplace retirement accounts (e.g., Roth or traditional IRA)

- Taxable brokerage accounts (e.g., Vanguard or Fidelity)

- Health Savings Accounts

- Insured accounts that sacrifice returns for safety (e.g., savings accounts, CDs, and money market funds)

Net Worth

Net worth—assets less liabilities—is a critical number for two reasons. First, it’s a great scorecard. If your net worth is increasing every year, odds are you’re handling your finances wisely. If it isn’t, odds are you’re a financial moron and you need to seriously reassess how you do personal finance. Second, you need to know your net worth in order to calculate your years to FI (see the next section of this post).

Quick aside. I butt-published this post a couple of times before I actually finished it. And the last time I butt-published it, The Crusher commented (see the date of his comment below) and made an interesting point about the effects of a primary residence on one’s net worth. Historically, a house returns roughly 3 percent annually while the stock market returns roughly 9 percent annually. If one’s house is a large percentage of one’s net worth, the growth of one’s net worth will lag behind the stock market’s growth. The takeaway, then, is this: If your house is a large percentage of your net worth, you need to lower the interest rate in the Years-to-FI Calculator below. If your house is 50 percent of your net worth, an interest rate of 6 percent is much more reasonable than an interest rate of 9 percent.

Years to FI

Okay, you know your monthly expenses, your monthly savings, and your net worth. Now you just have to know how many years of toil you have left. The good news is that in order to calculate your years-to-FI, you need to know your monthly expenses, your monthly savings, and your net worth. The bad news is that that calculation isn’t derived from a handy-dandy little formula such as the Pythagorean Theorem.

My goal was to create a simple in-house form for you to use, much like my MRI-RI Calculator. But the key to my proposed Years-to-FI Calculator was an Excel function called the NPER Function, and the math behind that function was difficult to find and impossible to incorporate. So rather than scrap my Years-to-FI Calculator altogether and just direct you toward Excel and the NPER Function, I decided to craft an Excel-based Years-to-FI Calculator myself and make it available for download.

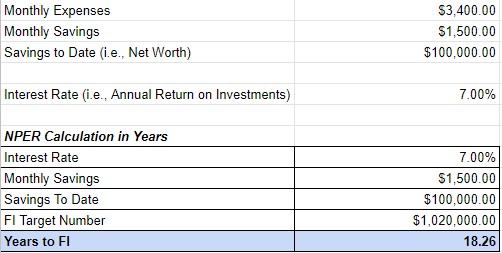

The screenshot below shows my Years-to-FI Calculator in action. I plugged in three of my four must-know FIRE numbers and picked a reasonable rate of return for my portfolio. The table in the bottom portion of my Years-to-FI Calculator did the rest.

If you spend $3,400 a month, your FI target number is $1,020,000. If you’ve already saved a hundred grand toward that target and invest $1,500 a month, you’ll need roughly 18 years and three months to reach FI.

Your years-to-FI can be reduced by lowering your monthly expenses or increasing your monthly savings. Your years-to-FI can also be reduced by assuming a higher return on your investments. I would caution against doing this, however, because you have no control over what returns the market will provide. Better to err on the side of caution (i.e., pick a return slightly less than the historic average) and be pleasantly surprised than to expect rosy returns and be profoundly disappointed. But that’s up to you. Anyway, download my Years-to-FI Calculator and play around with it. It’s a crude but helpful tool.

Quick aside. My Years-to-FI Calculator doesn’t account for inflation. But this shouldn’t be too much of a problem. As long as your income and savings keep pace with inflation, your years-to-FI number should be fairly accurate. Also, it wouldn’t hurt if you used this calculator once a year with updated numbers. Do that and you’ll render inflation a non-factor.

Final Thoughts

Okay, groovy freedomist, that’s all I got. What say you? Are my four FIRE-related numbers absolutely necessary to know if one wants to hobnob with FIRE enthusiasts and retain one’s self-respect? Or are my four FIRE-related numbers unmitigated piffle that should be ignored with extreme prejudice? Let me know what you think when you get a chance. Peace.

Leave a Reply