This post may contain affiliate links. Please read our disclosure for more information.

A few months back I came across a company called the Lending Club. And from what I read, it struck me as having a very intriguing business model. Here’s how the Lending Club works.

- Potential borrowers with relatively small loan requirements join the Lending Club (average loan size is $14,553).

- The Lending Club determines the riskiness of these potential borrowers and makes loans to those it deems to be an acceptable risk.

- Investors who join the Lending Club fund the loans that the Lending Club makes.

- Investors make money on the interest charged to borrowers.

- The Lending Club makes money by charging investors a 1 percent fee on every monthly payment a borrower makes (a $100 monthly payment, for instance, would generate $99 for investors and $1 for the Lending Club).

- If the Lending Club screws up and completely misjudges the credit-worthiness of its borrowers, investors and the Lending Club lose money.

In a nutshell, the Lending Club is the Uber of small-loan banking; it’s connecting people who need something (in this case, small loans) with people who want to provide that something (for a profit, of course).

I brought the Lending Club to the attention of Mrs. Groovy and we both agreed it might be worth a try. Perhaps we would invest $5,000-$10,000 in grade-A loans. Grade-A loans returned about 5 percent. That’s much better than what our bond funds were (and are) returning.

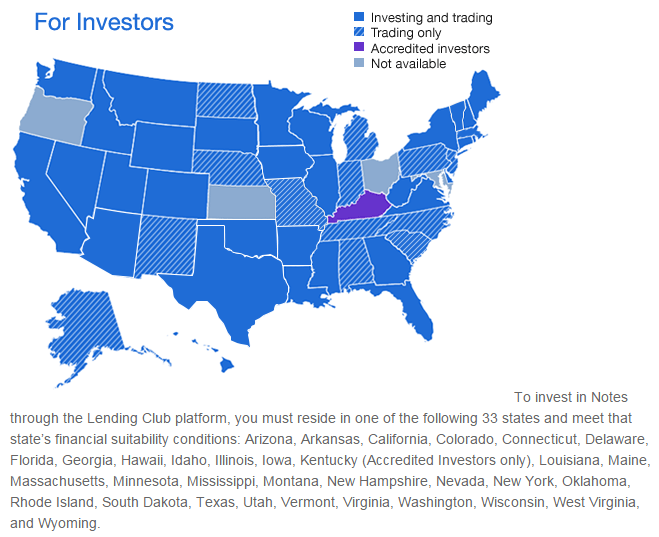

So, somewhat excitedly, I went to the Lending Club’s website and began the process of setting up an investor account. But there was a problem. I live in North Carolina. And the Tar Heel state doesn’t allow its citizens to be investors with the Lending Club. It’s illegal (see to the left the chart copied from the Lending Club’s website).

So, somewhat excitedly, I went to the Lending Club’s website and began the process of setting up an investor account. But there was a problem. I live in North Carolina. And the Tar Heel state doesn’t allow its citizens to be investors with the Lending Club. It’s illegal (see to the left the chart copied from the Lending Club’s website).

I was pissed. I can go online and legally buy an AR-15 assault rifle. No questions asked. If I were a pregnant 16-old-girl, a minor, I could legally, with neither the consent nor knowledge of my parents, contract the services of an abortionist. Again, no questions asked. But throw $5,000 at the Lending Club business model? Hell no. North Carolina can’t allow consenting adults to engage in money-lending. That would be as unseemly as “dogs and cats living together”, for heaven’s sake!

Why? Why can’t I risk $5,000 with the Lending Club?

Is it more risky than purchasing an assault rifle or getting an abortion?

One could argue that investing isn’t a constitutional right but possessing assault rifles and access to abortions are. Granted, the Constitution does give us the right to bear arms. But it says nothing about a right to abortions. In order to see that right in the Constitution, you have to put on your penumbra glasses. Only then can you see that abortions are protected by the equally invisible right-to-privacy clause. But if abortion is a privacy issue, why isn’t investing with the Lending Club a privacy issue? After all, what business is it of yours and anyone else if I want to lend money to someone at a modest interest rate and have the Lending Club be the matchmaker?

The point of this post isn’t to debate the merits of gun rights or reproductive rights. So I don’t want you to get sidetracked by those two emotional issues. I’m just trying to wrap my brain around this conundrum. Why are two commercial transactions, seemingly fraught with risk for the consumers involved and society at large, permissible, and one commercial transaction, seemingly with little or no risk to the consumer involved and society at large, not permissible? I guess if something isn’t deemed a constitutional right, the government, be it on the federal or state level, can decide who can avail themselves to it and who can’t. Some animals are more equal than others.

We’re in some dangerous territory here. Risk-taking is essential to freedom. Think about what the risk-taker is saying with his or her actions. He or she is saying that conventional wisdom is wrong; that he or she knows a better way and wants to prove it. Isn’t this how individuals and societies grow—by individuals experimenting, foregoing what’s comfortable, and exposing themselves to the possibility of ridicule and failure? And how free are we if we need permission from the government to challenge the status quo?

My inability to join the Lending Club as an investor is a trivial affront to liberty. But this trivial affront is far from isolated. Government is obsessed with “protecting” us from risk.

Want to buy a car directly from GM, Ford, or Chrysler? Not going to happen. You need the protection of a middleman (i.e., a car dealership). Want to use Uber? Maybe. As long as the city you’re in thinks it’s safe for you to be chauffeured by a contractor who hasn’t passed a state-approved background check. Want to be a DIY lawyer and prepare for the bar exam without college? No. For your own good you must attend seven years of college and have at least 100K in student loan debt before you can take the bar exam. Want a factory job? Forget about it. Building factories here will enlarge America’s carbon-footprint. And you don’t want that. You’ll be much safer from global warming if factories are built in China or Mexico instead. Want to opt out of Social Security at the start of your working career and use the savings from your reduced FICA taxes to supercharge your own retirement savings? Don’t make me laugh.

If one sentence can sum up the decline of America it is this: Death by a thousand little protections.

So get used to it, America. No risk-taking means no advancement for our country and no worries for entrenched powers. Everything that sucks (think healthcare, banking, education, the economy, border security, etc.), will continue to suck. Forever.

Any chance our esteemed members of the Supreme Court can find a right to take some freakin’ risks in those constitutional penumbras they’re always ruminating on?

Leave a Reply to Brian Stephens Cancel reply