This post may contain affiliate links. Please read our disclosure for more information.

As one’s income grows, so does one’s happiness. But this dynamic isn’t immune to the laws of diminishing returns. At an income of $75,000, happiness supposedly peaks.

Don’t ask me why, but my fertile mind got hung up on this factoid recently. On one hand, the correlation between income and happiness makes perfect sense. Make more money, have more money for necessities and frivolities, experience more happiness. Scarcity becomes less of a reality and the mind is freed from a major source of unhappiness: worry.

On the other hand, however, I know from personal experience that income and happiness aren’t perfectly correlated. In 2007, my income dropped over 40 percent and my happiness didn’t crater. In fact, the opposite occurred. I went from making $76,000 in New York to making $43,000 in North Carolina, and, yet, despite this $33,000 pay cut, my happiness meter jumped from run-of-the-mill happy to zippity-f*cking-doo-dah happy.

So what gives? Income is surely important when it comes to happiness. But it’s not the only thing. Something else is at play. Here are my thoughts.

The Keys to Happiness

Assuming for the moment that you’re physically and mentally healthy, socially and technically competent enough to secure friendship, love, and work, free from confinement, and happily untouched by unspeakable tragedy, here are the two things that will determine your happiness.

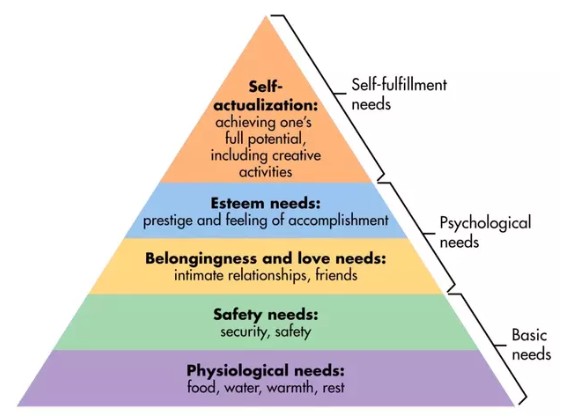

Personal Maslow

Here is Abraham Maslow’s hierarchy of human needs. Fail to secure any of these needs, especially those at the bottom of the pyramid, and you won’t be a happy camper.

But everybody’s maslow is different. When I was living in New York making $76,000 a year, my psychological needs were more than covered. (How couldn’t they be? I was married to the fabulous Mrs. Groovy, after all). But there were problems regarding basic needs and self-fulfillment needs.

I snore like an ogre. Mrs. Groovy and I can’t sleep in the same room. And this proved to be a big problem back in New York because Mrs. Groovy and I were living in a one-bedroom condo. Sleeping on the living-room sofa was miserable.

I also have a burning desire to tinker and create. A workshop, in turn, goes a long way toward fulfilling this desire. But back in New York, I didn’t have a workshop. Our one-bedroom condo had a community pool. It didn’t have a community workshop.

Once Mrs. Groovy and I relocated to North Carolina, however, my maslow improved dramatically. I was making significantly less money, but I had my own bedroom and bed, and I had my own workshop. And I still had Mrs. Groovy, of course. When it came to basic needs, psychological needs, and self-fulfillment needs, I was kicking ass.

Financial Competency

For our purposes here, financial competency will be defined as follows:

You can save 20 percent or more of your take-home pay.

This is a crude measure of financial competency for sure. Just because you’re a good saver doesn’t mean you’re a good investor. But it does show if you’re skilled or not at living below your means. It’s also income agnostic. The well-heeled aren’t assured victory. Someone making $50,000 a year can actually be more financially competent than someone making $500,000 a year.

Financial competency is key to happiness because it’s key to mitigating worry. Save enough money to handle a major car repair, a visit to the emergency room, or a prolonged job loss and you will have few sleepless nights.

The last year Mrs. Groovy and I were living in New York, we were saving roughly $2,000 a month. Since we were taking home $6,500 a month back then, we had a 30 percent savings rate. Pretty damn good. We had clearly achieved financial competency. But things would get much better once we relocated to North Carolina. Even though our household income took a big hit, our maslow issues were resolved and our savings rate jumped to 50 percent. Not surprisingly, worry went way down and happiness went way up.

Are More Variables Needed?

Without a doubt there are more variables to consider when it comes to happiness. Financial independence, for instance, just about slays the worry monster and gives one complete ownership of one’s time. But how realistic is financial independence for most Americans, and how much does it boost one’s happiness anyway? I was happier once I achieved financial independence, but not outrageously so. If I had to guess, FI Mr. Groovy was 10 to 15 percent happier than pre-FI Mr. Groovy.

No, for the average joe and josephine out there, the happiness riddle boils down to Maslow’s hierarchy and financial competency. Get your maslow right and save 20 percent of your take-home pay and you will very likely achieve 80 to 85 percent of the happiness you’re capable of.

Final Thoughts

Okay, groovy freedomist, that’s all I got. What say you? Income is an important variable when it comes to one’s happiness. But I believe that fixing your maslow and achieving financial competency are even more important variables. Am I onto something? Or am I needlessly complicating this happiness thing? Let me know what you think when you get a chance. Peace.

Leave a Reply to Mr. Groovy Cancel reply